I think this is Ackman's second investment with Franklin - Burggruen. The first was in Justice Holdings, which ended up buying Burger King and is now listed on the NYSE (and Ackman still owns). He was a co-founder of Justice, but at Platform he is just an investor; after the relisting on the NYSE, Pershing Square will have a representative on the board.

This is certainly not Twitter, but a new listing to take a look at.

Liberty and Freedom

Franklin - Burggruen had some other SPACs too in the past. Two of them were U.S. listed; Liberty Acquisition which I suppose we can call a disaster and Freedom Acquisition. The other one, Liberty Acquisition International was listed (like Justice and Platform) in Europe, so I am not too familiar with that one.

I only looked at the two U.S. listed ones (at the time); Liberty Acquisition merged with Prisa; I remember reading about it at the time and I wasn't comfortable at all with it as it was an entity in Europe and I had no familiarity with it. Freedom Acquisition acquired (or merged with) GLG, a hedge fund manager. I looked at that too and wasn't particularly interested in GLG.

I don't know much about Nicolas Burggruen other than what I read in the press; that he is a homeless billionaire (living in hotel rooms), so I can't say anything about his style or philosophy.

Anyway, I suppose someone might have done an IRR on the above SPACs, but I don't have those handy with me (But as you will see, even though that is important, I am sort of interested in what Platform just bought).

Martin Franklin is well-known to U.S. investors because of his work at Jarden Corp (JAH). He sort of does fit the outsider CEO mold (prudent acquisition driven growth). JAH is certainly a candidate for a post here on this theme I seem to be on here these days.

Martin Franklin took over JAH as Chairman and CEO in September 2001 and now is executive chairman (gave up CEO post in 2011).

For those who don't know him, check this out:

Jarden Corp Stock Price Performance Since September 2001

Returns since September 2001:

JAH: +33.5%/year (total return)

S&P 500 index: +4.6%/year (excluding dividends)

Berkshire Hathaway: +7.8%/year

Ackman's interest in investing with Martin Franklin is clearly due to his performance at JAH (that's exactly what he said).

Platform Specialty Products

So anyway, the fact that PAH (Platform Acquisition Holdings, listed in London but trading halted due to deal) is a SPAC started by Martin Franklin and Nicolas Burggruen is enough to be interesting. But I generally don't invest in SPACs, even with reputable founders. There was a time when it was a free call option; you can buy them at book or a discount and then vote either way on an acquisition; if it is voted down (or you choose to), you can get your cash back. If not and the acquisition is sweet, then you make money on the pop.

In fact, the Special Opportunities Fund (SPE) owns a basket of SPACs and SPAC warrants as a sort of cheap option on good acquistions. It's certainly a good idea, but for me, I just tended to think that this SPAC trade was a sort of pre-crisis thing. Since it was basically an arbitrage between private market values and public market values, maybe this trade is getting more interesting again; public market valuations are up a lot in the last couple of years. So maybe this 'pop' will start to come back. In the past few years, public market prices tended to look cheap and private market prices seems to have gone up due to the private equity boom.

Crumbs and American Apparel are two SPACs that come to mind that have been disasters. I'm sure there have been some great ones, but I'll leave that game to others. I'm too lazy to find things that pop; I want to find long term places to put my money (of course, owning SPE will give you some of that exposure!).

In any case I did have Platform Acquisition at the back of my mind but it wasn't really a priority for me to look at. But thanks to a commentor in the POST post (no pun intended), I had to front-burner this because:

The business Platform Acquisition bought might be an outsider CEO company.

Platform Acquisition, in October (closed in November), bought MacDermid, a specialty chemical company. They will change the name of Platform Acquisition to Platform Specialty Products and relist on a U.S. stock exchange.

MacDermid an Outsider CEO Company?

MacDermid was a publicly traded company until 2007 when there was a managment buyout. The MBO happened at $1.3 billion, or around 9x EV/EBITDA. The Platform acquisition happened at 10x adjusted EBITDA (at $1.8 billion). So the valuation looks more or less in line with what management thought it was worth back in 2007 (OK, 9 is not 10, but close enough for the blogoshpere!).

But first, let's look at what raised my eyebrows. MacDermid is run (and has been run since 1990) by Daniel Leever (65 years old so not young, but not too old either!).

On the investor conference call when the acquistion was announced, they said that during Daniel Leever's tenure, MacDermid increased revenues five times. He has been with MacDermid for 34 years and has been CEO for 24 years. I assume his "tenure" is the time he was CEO. That's a modest 7%/year in revenue growth; 5x in 24 years = 7%/year.

They said he increased the value of the company from $80 million to the current $1.8 billion through those years. So that's +13.9%/year since 1990. Not bad at all. I think they said he increased market cap or equity value 30x during his tenure. Assuming that means 1990-now, that's +15%/year. This growth includes acquisitions, but no equity raises.

Although pretty good, it's not quite up to par of the original "outsiders". Here, look:

1. Tom Murphy (Capital Cities Broadcasting):

+19.9%/year over 29 years versus +10.1%/year for the S&P 500 index

2. Henry Singleton (Teledyne):

+20.3%/year over 27 years versus +8.0%/year for the S&P 500 index

3. Bill Anders (General Dynamics)

+23.3%/year over 17 years versus +8.9%/year for the S&P 500 index

4. John Malone (TCI)

+30.3%/year over 25 years (up to ATT acquisition) versus +14.3%/year for the S&P 500 index

5. Katharine Graham (The Washington Post)

+22.3%/year over 22 years (since IPO) versus 7.4%/year for the S&P 500 index

6. Bill Stiritz (Ralston Purina)

+20.0%/year over 19 years versus +14.7%/year for the S&P 500 index

7. Dick Smith (General Cinema)

+16.1%/year over 43 years versus +9%/year for the S&P 500 index

8. Warren Buffett (Berkshire Hathaway)

+20.7%/year over 46 years (through 2011) versus 9.3% for the S&P 500 index

But then again, these guys are really special. You're not going to find a lot of these lying around.

Let's take a quick look at valuation.

Valuation

The MBO of MacDermid happened at around 9x EV/EBITDA. Since MacDermid was a publicly listed company, you can go to sec.gov and get 10-k's and other filings including the MBO merger proxy from 2007. I was going to use that proxy for valuation, but there is a more recent proxy from the Solutia acquisition by Eastman in early 2012. There is probably a more recent acquisition/merger, but this is good enough for comparative transaction analysis. Since this is not a Conde Naste publication and I don't have free interns working for me, I will do the comparative company analysis myself.

Anyway, here is some info from the Solutia merger proxy (dated May 2012, analysis by Deutche Bank and Moelis):

Date

|

Bidder

|

Target

|

Consideration

|

Total

Enterprise

Value ($ billion) | ||||

Core Selected

Transactions

|

||||||||

July

2011

|

Lonza

Group Ltd

|

Arch Chemicals, Inc.

|

Cash | 1.4 | ||||

May

2011

|

Ashland

Inc.

|

International

Specialty Products Inc.

|

Cash | 3.2 | ||||

April

2011

|

Solvay

S.A.

|

Rhodia

S.A.

|

Cash | 7.3 | ||||

March

2011

|

Berkshire

Hathaway Inc.

|

The

Lubrizol Corporation

|

Cash | 9.6 | ||||

July

2008

|

Ashland

Inc.

|

Hercules

Inc.

|

Cash and Stock | 3.4 | ||||

April

2004

|

The

Lubrizol Corporation

|

Noveon

International, Inc.

|

Cash | 1.8 | ||||

Other Selected

Transactions

|

||||||||

October

2011

|

American

Securities LLC

|

Unifrax

I LLC

|

Cash | 0.9 | ||||

July

2011

|

Ecolab

Inc.

|

Nalco

Holding Company

|

Cash or Stock | 8.1 | ||||

June

2010

|

BASF

SE

|

Cognis

Holding GmbH

|

Cash | 3.2 | ||||

September

2008 |

BASF

SE

|

Ciba

Holding AG

|

Cash | 5.0 | ||||

July

2008

|

The

Dow Chemical Company

|

Rohm

and Haas Company

|

Cash | 18.9 | ||||

Date

|

Bidder

|

Target

|

Consideration

|

Total

Enterprise

Value ($ billion) | ||||

August

2007

|

Akzo

Nobel N.V.

|

Imperial

Chemical Industries PLC

|

Cash | 10.7 | ||||

May

2007

|

Saudi

Basic Industries Corporation

|

GE

Plastics business of General Electric Company

|

Cash | 11.6 | ||||

September

2006 |

Court

Square Capital Partners II, L.P. / Weston Presidio V, L.P. /

Management

|

MacDermid

Incorporated

|

Cash | 1.3 | ||||

September

2006 |

Apollo

Management L.P.

|

GE Advanced Materials

business of General

Electric

Company

|

Cash and Stock | 3.8 | ||||

February

2006 |

BASF

SE

|

Construction

Chemicals business of Degussa AG

|

Cash | 3.2 | ||||

March

2005

|

Texas

Pacific Group

|

British

Vita PLC

|

Cash | 1.3 | ||||

March

2005

|

Crompton

Corp.

|

Great

Lakes Chemical Corporation

|

Stock | 1.8 | ||||

February

2005 |

Cytec

Industries Inc.

|

Surface

Specialties business of UCB SA

|

Cash | 1.8 | ||||

July

2004

|

Apollo

Management

|

Borden

Chemical Inc.

|

Cash | 1.1 |

With respect to each selected transaction

and based on publicly available information, Solutia’s financial advisors

calculated the multiples of the target’s total enterprise value to its EBITDA

for the twelve-month period prior to announcement of the applicable transaction,

which is referred to below as “TEV / LTM EBITDA.”

This analysis indicated the following:

Selected Transactions TEV/LTM EBITDA

Multiples

| High | Mean | Median | Low | |||||||||||||

Core

Selected Transactions

|

9.2x | 8.3x | 8.7x | 6.9x | ||||||||||||

Other

Selected Transactions

|

12.4x | 9.3x | 9.3x | 6.1x | ||||||||||||

All

Transactions

|

12.4x | 9.0x | 9.0x | 6.1x | ||||||||||||

So anyway, this analysis includes transactions between 2004 and 2011 so includes a lot of deals. The core selected group deals were done at a mean of 8.3x EV/LTM EBITDA which looks lower than the current MacDermid deal. For all transactions, the multiple is 9.0x. Platform paid 10.0x last twelve months adjusted EBITDA so looks higher than previous deals.

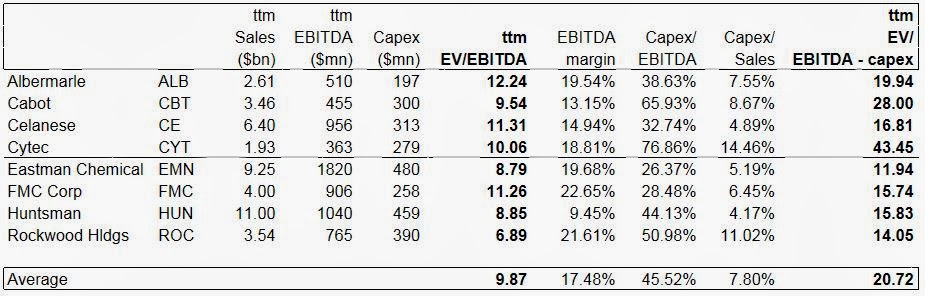

The comparative listed valuations in the 2012 proxy for Solutia is a little dated since the market has done very well since early 2012, so here is my quick update on the listed comps. I just took the last twelve month figures, EV and things like that from Yahoo Finance.

Publicly Listed Comps (Specialty Chemicals)

This is the same universe of comps that was in the Solutia proxy. It looks like specialty chemicals trade at around 10x EV/EBITDA, so the deal price is within range of where specialty chemicals trade these days.

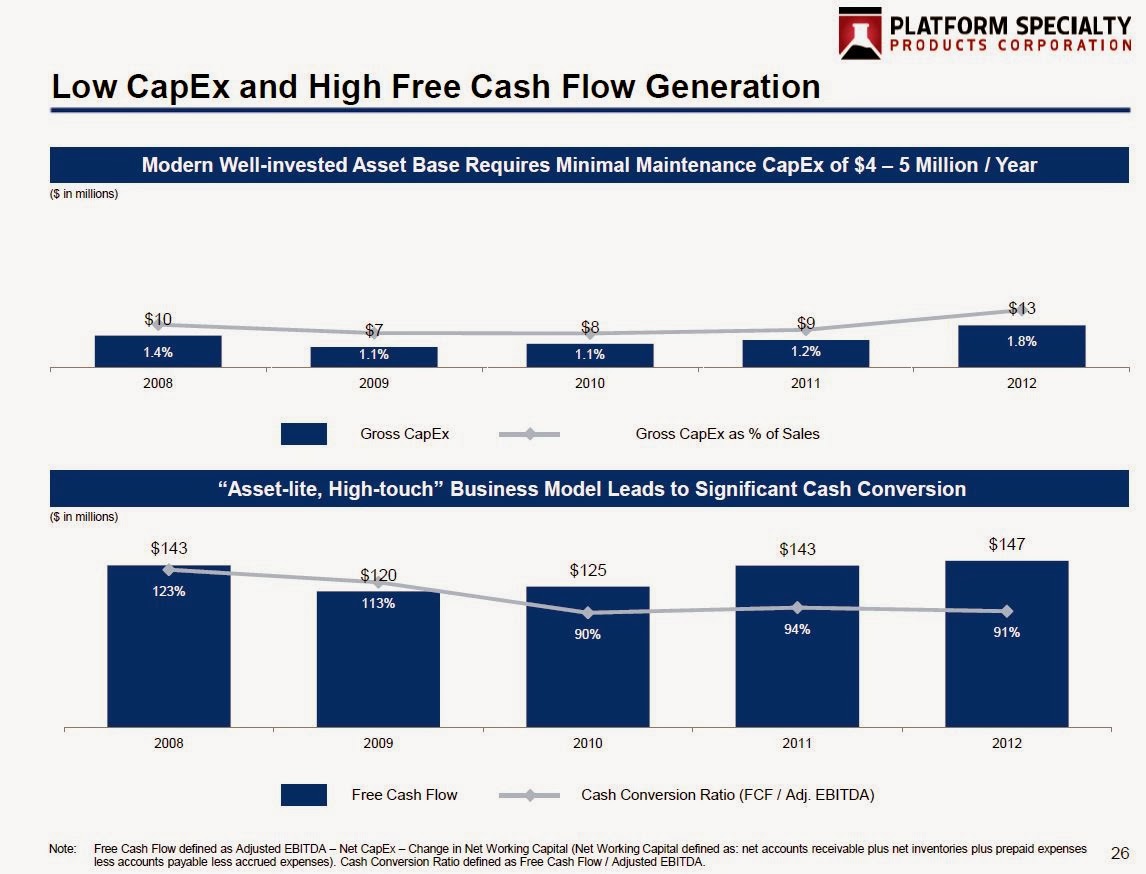

But here's the interesting thing. McDermid is asset-lite and has very little capex; they generate a lot of free cash (sound familiar?). Here's a slide from their recent presentation:

If they are generating 90 cents of free cash (unlevered, pretax) per $1.00 of EBITDA, then a 10x EV/EBITDA might be pretty cheap. With 90% cash conversion, then a 10x EV/EBITDA translates into a 11x EV/(EBITDA-Capex).

The table above shows that EV/(EBITDA-Capex) for specialty chemicals averages 21x. Average capex to sales is 8% versus less than 2% at MacDermid. Free cash conversion is only a little over 50% at other specialty chemicals versus over 90% for MacDermid. So on that basis, it looks like a good deal.

Cumulative Preferreds

MacDermid planned on doing an IPO in 2011 / 2012 so they filed an S1 (and many amendments). It's a good summary of what MacDermid is about.

One thing jumped out at me that shouldn't be an issue going forward. As part of the MBO in 2007, they issued payment-in-kind cumulative preferreds shares. This is from the S1 that shows how much the preferred owners are getting (or accruing):

| Year ended December 31, | Three months ended March 31, | |||||||||||||||||||

| 2011 | 2010 | 2009 | 2012 | 2011 | ||||||||||||||||

| (amounts in thousands) | (unaudited) | |||||||||||||||||||

Statement of Operations Data:

| ||||||||||||||||||||

Net sales

| $ | 728,773 | $ | 694,333 | $ | 594,153 | $ | 182,195 | $ | 178,521 | ||||||||||

Cost of sales

| 388,298 | 371,223 | 333,963 | 95,884 | 94,980 | |||||||||||||||

Gross profit

| 340,475 | 323,110 | 260,190 | 86,311 | 83,541 | |||||||||||||||

Operating expenses:

| ||||||||||||||||||||

Selling, technical and administrative

| 185,649 | 179,786 | 156,508 | 45,746 | 45,629 | |||||||||||||||

Research and development

| 22,966 | 21,005 | 20,103 | 6,718 | 5,359 | |||||||||||||||

Amortization

| 28,578 | 29,694 | 29,868 | 6,655 | 7,362 | |||||||||||||||

Restructuring(1)

| 896 | 6,234 | 4,228 | 114 | (181 | ) | ||||||||||||||

Impairment charges(2)

| 46,438 | — | 68,692 | — | — | |||||||||||||||

Total operating expenses

| 284,527 | 236,719 | 279,399 | 59,233 | 58,169 | |||||||||||||||

Operating profit (loss)

| 55,948 | 86,391 | (19,209 | ) | 27,078 | 25,372 | ||||||||||||||

Other income (expense):

| ||||||||||||||||||||

Interest income

| 500 | 696 | 458 | 175 | 108 | |||||||||||||||

Interest expense(3)

| (54,554 | ) | (56,196 | ) | (60,740 | ) | (13,556 | ) | (14,088 | ) | ||||||||||

Miscellaneous income (expense)(4)

| 9,412 | 15,106 | (5,020 | ) | (4,353 | ) | (16,172 | ) | ||||||||||||

Income (loss) from continuing

| 11,306 | 45,997 | (84,511 | ) | 9,344 | (4,780 | ) | |||||||||||||

Income tax (expense) benefit(3)

| (9,953 | ) | (21,723 | ) | 6,427 | (4,366 | ) | (1,145 | ) | |||||||||||

Income (loss) from continuing operations

| 1,353 | 24,274 | (78,084 | ) | 4,978 | (5,925 | ) | |||||||||||||

(Loss) income from discontinued operations, net of tax(5)

| — | — | (4,448 | ) | — | — | ||||||||||||||

Income (loss) from continuing operations

| 1,353 | 24,274 | (82,532 | ) | 4,978 | (5,925 | ) | |||||||||||||

Less net income attributable to the non-controlling interest

| (366 | ) | (343 | ) | (295 | ) | (91 | ) | (88 | ) | ||||||||||

Net income (loss) attributable to MacDermid, Incorporated

| 987 | 23,931 | (82,827 | ) | 4,887 | (6,013 | ) | |||||||||||||

Accrued payment-in-kind dividend on cumulative preferred shares

| (40,847 | ) | (37,361 | ) | (34,124 | ) | (10,788 | ) | (9,874 | ) | ||||||||||

Net (loss) attributable to common shares

| $ | (39,860 | ) | $ | (13,430 | ) | $ | (116,951 | ) |

$

|

(5,901

|

)

| $ | (15,887 | ) | |||||

From the balance sheet:

Stockholders’ Equity

| ||||||||||||

Cumulative preferred shares, 316,000 shares authorized and issued, 315,254 shares outstanding at March 31, 2012 and 315,264 shares outstanding at December 31, 2011, respectively, including cumulative dividends of $175,237 and $164,449 at March 31, 2012 and December 31, 2011, respectively

| $ | 491,237 | $ | 480,449 | — | |||||||

Common shares, 50,000,000 shares authorized and issued, 9,946,140 shares and 9,946,439 shares outstanding at March 31, 2012 and December 31, 2011, respectively

| 50,000 | 50,000 | 314 | |||||||||

Class A Junior shares, 430,000 shares authorized and issued, and 314,245 vested shares and 314,245 vested shares outstanding at March 31, 2012 and December 31, 2011, respectively

| — | — | — | |||||||||

Class B Junior shares, 324,000 shares authorized and issued, and 100,156 vested shares and 49,878 vested shares outstanding at March 31, 2012 and December 31, 2011, respectively

| — | — | — | |||||||||

Additional paid-in capital

| 2,254 | 2,156 | 542,171 | |||||||||

Accumulated deficit

| (280,359 | ) | (274,458 | ) | (280,359 | ) | ||||||

Accumulated other comprehensive income

| (9,261 | ) | (14,959 | ) | (9,261 | ) | ||||||

Common and preferred shares in treasury, 746 preferred shares and 736 preferred shares and 53,860 common shares and 53,561 common shares at March 31, 2012 and December 31, 2011, at cost, respectively

| (1,006 | ) | (994 | ) | — | |||||||

Total Stockholders’ equity

| 252,865 | 242,194 | 252,865 | |||||||||

Equity (deficit) in non-controlling interest

| 69 | (388 | ) | |||||||||

Total equity

| 252,934 | 241,806 | ||||||||||

Total liabilities and equity

| $ | 1,232,981 | $ | 1,221,418 | ||||||||

See accompanying notes to consolidated financial statements.

This looks really scary and unacceptable, but if the IPO happened, these cumulative preferreds would have been converted to common equity so on a pro-forma basis, those cumulative dividend accruals wouldn't be there (and wouldn't recur in the future).

The recent presentation doesn't include a detailed balance sheet so I don't know if these preferreds are still outstanding. If they are, I would assume that these preferreds will be converted into common equity.

The accumulated deficit of $280 million looks very un-outsider CEO-like. But much of this is MBO related; up until the end of 2006, it looked like a normal company (from their 2006 10-K):

Twelve Months Ended December 31,

| |||||||||||

2006

|

2005

|

2004

|

2003

|

2002

| |||||||

OPERATING RESULTS:

| |||||||||||

Net sales

|

$817,609

|

$738,043

|

$660,785

|

$619,886

|

$611,490

| ||||||

Earnings from continuing operations before cumulative effect of accounting change

|

$51,850

|

$47,043

|

$53,224

|

$49,820

|

$31,477

| ||||||

Earnings (loss) from discontinued operations, net of tax

|

—

|

—

|

—

|

5,592

|

(22,128

|

)

| |||||

Cumulative effect of accounting change, net of tax

|

—

|

—

|

—

|

1,014

|

—

| ||||||

Net earnings

|

$51,850

|

$47,043

|

$53,224

|

$56,426

|

$9,349

| ||||||

Basic earnings per common share:

| |||||||||||

Continuing operations

|

$1.68

|

$1.55

|

$1.76

|

$1.60

|

$0.98

| ||||||

Discontinued operations

|

—

|

—

|

—

|

0.18

|

(0.69

|

)

| |||||

Cumulative effect of accounting change

|

—

|

—

|

—

|

0.03

|

—

| ||||||

Net earnings

|

$1.68

|

$1.55

|

$1.76

|

$1.81

|

$0.29

| ||||||

Diluted earnings (loss) per common share:

| |||||||||||

Continuing operations

|

$1.66

|

$1.52

|

$1.72

|

$1.59

|

$0.98

| ||||||

Discontinued operations

|

—

|

—

|

—

|

0.18

|

(0.69

|

)

| |||||

Cumulative effect of accounting change

|

—

|

—

|

—

|

0.03

|

—

| ||||||

Net earnings

|

$1.66

|

$1.52

|

$1.72

|

$1.80

|

$0.29

| ||||||

Restated(1)

|

Restated(1)

|

Restated(1)

|

Restated(1)

| ||||||||

FINANCIAL POSITION AT YEAR END:

| |||||||||||

Total assets

|

$924,681

|

$819,927

|

$793,427

|

$709,794

|

$708,873

| ||||||

Long-term debt (including short-term portion)

|

$300,851

|

$301,275

|

$301,341

|

$301,761

|

$316,467

| ||||||

Shareholders’ Equity

|

$414,671

|

$339,077

|

$323,740

|

$251,570

|

$218,718

| ||||||

SHARE DATA:

| |||||||||||

Cash dividends declared per common share

|

$0.24

|

$0.24

|

$0.16

|

$0.10

|

$0.08

|

From the balance sheet:

Shareholders’ equity

| |||||||||||

Common stock, authorized 75,000,000 shares, issued 47,686,761 at December 31, 2006 and 47,131,950 shares at December 31, 2005, at stated value of $1.00 per share

|

47,687

|

47,132

| |||||||||

Additional paid-in capital

|

57,584

|

42,869

| |||||||||

Retained earnings

|

411,261

|

366,807

| |||||||||

Accumulated other comprehensive income (loss)

|

22,924

|

(3,051

|

)

| ||||||||

Less—cost of common shares held in treasury, 16,845,198 at December 31, 2006 and 16,546,763 at December 31, 2005

|

(124,785

|

)

|

(114,680

|

)

| |||||||

Total shareholders’ equity

|

414,671

|

339,077

| |||||||||

Total liabilities and shareholders’ equity

|

$

|

924,681

|

$

|

819,927

| |||||||

|

But if you look through the capital structure issues and just focus on the operations, it looks fine.

Great Annual Reports

I just read through the annual reports from 1994-2006 which are available at sec.gov. I wasn't familiar with MacDermid at all when it was listed, but the annual reports are really well-written. They are inspired by Warren Buffett.

Here's a snip from the 1998 annual report:

Nineteen ninety-eight was an eventful year. After 60 years of

inspirational leadership Harold Leever, our Chairman, has chosen to become

Chairman Emeritus. He will continue as a Director. What a ride! In 1959

Harold, with a number of employees, bought out MacDermid's founder, Archie

MacDermid. In the early '60s, in what turned out to be a brilliant

strategic move, he led a tiny metal finishing cleaner company into the

electronic chemical business. This was a huge bet at the time, and we are

still enjoying its fruits today. Perhaps more importantly, Harold

established the MacDermid Philosophy. It is printed as usual on the

inside front cover of this report (before the numbers). Today the "Clan

MacDermid" with over a thousand members in 19 countries around the world

is as focused as ever on the Philosophy's core principles:

focus on the customer honesty and integrity

supreme worth of the individual challenging and demanding environment

entrepreneurship teamwork and cooperation

Harold has been our spiritual leader for 60 years and will continue to be

forever. I hope you can join us to celebrate this milestone with Harold

and Ruth Ann at our annual meeting on July 22.

Another important event in 1998 was a non-event which we believe

defines who we are as clearly as what did occur. We entertained acquiring

a fairly large company that would have immediately added to earnings per

share. But, given our optimism about our internal growth prospects, we felt

the acquisition would dilute per share results several years out and thus

turned it down. We are focused on building long-term shareholder value.

While acquisitions can be and have been important, we will issue shares only

when we receive at least as much in business value as we give. Tomorrow

becomes today rather quickly. Not only is that our responsibility to you,

but it is in our own self interest. Your employees, through our investment

plans and options, own 35% of the company. Many, like myself, have the vast

majority of our net worth invested in the company.

I added the italics.

The shareholders' principles were plagiarized (Leever's term) from Berkshire Hathaway with the permission of Warren Buffett.

MACDERMID CORPORATE PHILOSOPHY

OUR BUSINESS

MacDermid Incorporated is in the international business of researching,

developing, acquiring, manufacturing, marketing, and servicing, for optimum

profit to us and our customers, specialty chemicals and systems for the chemical

treatment, surface preparation and finishing of metals, plastics and other

materials in accordance with accepted ecological and social considerations.

OUR CUSTOMERS

We will create an industry image that automatically causes people in the

industries we serve to think first of MacDermid.

We will justify their action by first thinking of the customers' needs ---

what's right for them makes it right for MacDermid --- by supplying a total

system including processes, know-how and services that assist in meeting all

their needs.

OUR PEOPLE

We continue to believe in the supreme worth of the individual and the

dignity of his or her work for the benefit of all. We will provide the

opportunity for our people to fulfill satisfactorily their own personal

objectives and ambitions and reward them in proportion to their contribution

toward achieving the Corporate objectives.

We will continue to be a place of opportunity where people "have the guts

to fail." We will encourage the entrepreneurs and innovators. We will

continually challenge the goals, objectives, organization and all the operating

and procedural aspects of our business and modify them when needed.

Our progress and your progress, our Company's long-term advantage and your

long-term advantage, lie in our human resources. Other advantages that come

about from technological improvements, the opening of new markets, lower costs,

etc., all prove to be relatively short run. So, basically, it is the initiative,

the will and the motivation that people bring to their work on which we rely for

our survival and growth.

We will continue to try to attract new people who have creative and probing

minds; people who will at times be disturbing -- questioning policy and

procedures. If we are wise, we will welcome it, resolve it, put it to work or

forget it.

We will continue to expand with the best possible talent available and

continue to train them, and ourselves, so that we each increase our ability to

contribute to the Company's progress.

We will each strive to exemplify the MacDermid Spirit of teamwork and

cooperation throughout the organization which has been instrumental to our past

and present growth as a corporation.

WHAT WE CAN EXPECT FROM YOU

First and foremost, we expect of you a fundamental honesty --- honesty with

yourself, with your Company and with all those with whom you interact, whether

they be associates within our organization, our customers or society in general.

Character and strength have always been born of honesty and a willingness to

face up to the truth of each situation as it arises.

Second, we expect and insist on hard work. An easy life, marked by the

absence of difficulty, builds neither character nor happiness. We believe that

self-realization of the individual is founded on accomplishment, which implies a

willingness to make the sacrifices necessary to get the job done the way it

should be done.

Third, we expect you to accept responsibility. Every assignment you will

have carries with it a responsibility for accomplishment. Commit yourself to

achievement which you consider beyond the scope of your talents and then program

your effort to translate it into a reality.

Fourth, we expect of you a loyalty --- loyalty to yourself, your family,

your associates, your organization and our customers. We have always worked

together as an organization and your own personal achievements will be measured

in terms of the contribution you make to our joint effort.

Fifth, we expect you to demonstrate good judgment. Judgment is essentially

an ability to appraise facts. Factual knowledge must come before good judgment.

This means you must continually educate yourself on our Company, our products

and our industry. In this way, you will have the material on which a sound

appraisal of good judgment is based.

This is what we expect of you, and being in an extremely competitive

environment, we have a real urgency in this expectancy.

WHAT YOU CAN EXPECT FROM US

One, you can expect from us the fairest treatment of which we are capable

--- fair in respect to matters of compensation, fair in respect to working

conditions and fair in respect to personnel policies.

Two, you can expect from us, as a Company, complete honesty in whatever we

do. Your assignments will never compromise the principles of honesty and common

decency which we also expect you, as an individual, to uphold.

Three, you can expect that we will provide assignments which will represent

challenges to you --- assignments which will enable you to grow toward your

professional and personal objectives.

Four, you can expect that we will offer opportunities for advancement. Our

desire is to grow from within.

Five, you can expect that we will be a demanding organization --- demanding

of your time, your talents and the best which you as an individual have to

offer. In this way our company will grow and you will grow with it.

Perhaps all this can best be summarized in these words from an unknown

author:

"Create mental pictures of your goals, then work to make those pictures become

realities.

Exercise your God-given power to choose your own direction and influence your

own destiny and try to decide wisely and well.

Have the daring to open doors to new experiences and to step boldly forth to

explore strange horizons.

Be unafraid of new ideas, new theories and new philosophies.

Have the curiosity to experimentto test and try new ways of living and

thinking.

Recognize that the only ceiling life has is the one you give it and come to

realize that you are surrounded by infinite possibilities for growth

and achievement.

Keep your heart young and your expectations high and never allow your dreams to

die".

MACDERMID SHAREHOLDER PRINCIPLES

1.OUR VISION IS TO BUILD ONE OF THE WORLD 'S GREATEST INDUSTRIAL COMPANIES

We believe that the excitement inherent in the culture of ultra high performance

will differentiate us from our competitors, who, while fine companies in their

own right, simply will find it impossible to keep up with the fighting Clan

MacDermid.

2.OUR FORM IS CORPORATE, OUR ATTITUDE IS PARTNERSHIP

Unlike many public companies, our employees and Directors own close to 33% of

the shares, so, we obviously think as owners. We hope that you consider your

investment in MacDermid as being a part owner of a business, much as you would

if you owned a small business in partnership with your close friend or family.

You would not be concerned about the evaluation of that small business weekly or

monthly. Many employees, including your CEO, have the vast majority of our net

worth in MacDermid stock. We intend to be very long term holders, thinking in

generational terms. We desire to partner with like-minded individuals and

institutions. We will not respond to short term pressures from the market.

3.WE FOCUS TO BUILD INTRINSIC VALUE,PER SHARE

We define intrinsic value as the present value of free cash flow, measured per

share. Cash flow will be invested in growth opportunities. We will build in

significant margin for error in investment assumptions. We have no interest in

top line growth for growth's sake. Per share cash flow is what counts. Our goal

is to increase per share intrinsic value by 25% per year. We believe in setting

stretch targets even though sometimes we may fall short of our goals.

4.PERSONAL AND CORPORATE RESPONSIBILITY

MacDermid will demonstrate the highest standards of personal and corporate

ethics and responsibility, with special emphasis on our environment. We take

seriously our leadership commitment to the communities in which we do business.

5.CARE OF OUR PEOPLE IS A TOP PRIORITY

We know to build one of the world's greatest industrial companies requires an

unusual partnership with the people charged with making the vision a reality. We

are guided by the MacDermid philosophy, including our clear statement of

commitment to our people, and our expectations of their commitment to MacDermid.

We maintain policies that encourage long, productive service. We avoid short

term policies like layoffs and restructuring simply to make the current quarter

or year numbers. That's not to say that we will not have reductions in staffing

based on performance, or if we feel the long term health of the business

requires us to do so. But even then we will do so with great reluctance. Our

people are our most important asset. We treat them as such by investing heavily

in training and education and management development.

6.LONG TERM INVESTMENT HORIZON

We will aggressively fund sound internal growth opportunities mostly in research

and market development regardless of short term impact. We will fund these

opportunities when the time is right, not necessarily when it is convenient. Our

internal investment opportunities normally offer an exceptional return, but

often require multi-year horizons. We will avoid the stop-start method of

investing, which is typical of a short term mentality.

7.LOW COST OPERATING STRUCTURE

We know that our ability to invest aggressively requires us to have a cost

structure lower than our competitors. Investing AND lowering our current costs

constantly is a core principle of our company.

8.HIGH OPERATING MARGINS

Growth opportunities will be passed through a margin filter prior to investment.

9.LOW CAPITAL EXPENDITURES

We invest shareholder funds in high return assets after a healthy margin for

error. Bricks and mortar have no attraction if they will not produce a high

return.

10.CAPITAL STRUCTURE

Cost of capital is an important consideration. Our ability to generate

relatively high amounts of cash allows us to carry significant debt while still

maintaining a healthy margin for error. We will issue common stock only when we

receive at least as much in intrinsic value as we give.

11.DIVIDENDS

Our current dividend is a result of history. Increasing our dividend is not a

high priority. We believe we can better serve shareholders by using internally

generated funds to grow the business or purchase shares.

12.ACCOUNTING

We will be candid in our reporting to you. We will tell you the business facts

that we would want to know if the positions were reversed, while safeguarding

information which would aid our competitors.

13.REPORTING

We will be communicating with you in several ways. Through our annual report, we

will try to give all shareholders as much value - defining information as

possible. At our annual meeting we will spend as much time as necessary to

provide information and answer questions. The forum section of our web site,

macdermid.com, provides shareholders the opportunity to submit questions

directly to the CEO. We will answer questions honestly and as promptly as

practicable. In all of our communications, we try to make sure that no

shareholder gets an edge. Our goal is to have all of our shareholders updated at

the same time.

14.FAIR VALUE

To the extent possible, we would like each MacDermid shareholder to record a

gain or loss in market value that is proportional to the gain or loss in

per-share intrinsic value. Obviously we cannot control MacDermid's share price

but by our policies and communications, over time we believe, are likely to

attract long term investors who seek to profit strictly from the progress of the

Company.

From the 2002 annual report

A COMMENT ON WEIGHING VS. VOTING: Many of our shareholders know we are long

time followers of what I call "Buffett Principles", taken from the business

philosophies of Warren Buffett. An important Buffett principle is, "In the

short term the stock market is a voting machine and in the long term it is a

weighing machine". This means that at any given point in time the market may

overreact in it's valuation of a particular stock, either too high or too low.

In the case of the late 90's bubble it overreacted towards the whole market.

Just because the market says the dot com is worth so much "per hit", it doesn't

mean it is so - long term. A business model that generates no cash over time is

valueless. Further this principle holds that over time, financial performance

and market value tend to converge. This principle is what drives our cash flow

discipline. Frankly I wouldn't take great comfort if I thought I had to depend

on Wall Street to "vote" on our relative success. Our cash flow in effect

allows us to take matters into our own hands. Here's an overly simple example.

Say we generate $60 million in free cash flow per year for the next ten years.

At the end of ten years we would have $600 million in cash in the bank. Today

our market cap is a little over $600 million. Do you think all else being

equal, our market value would still be $600 million, or equal to only the cash

in the bank? Not likely. Regardless of how depressed Mr. Market felt at the

time, one would assume the more objective 'weighing' would have to take over at

some point. Maybe a better way to look at it is as follows. Assume Mr. Market

was depressed for the whole 10 years, our stock price never moved, and we simply

took the cash and bought back our stock each year. In ten years there would be

one share left that generated $60 million in free cash! I think Mr. Market, no

matter how depressed he was, would offer more than $20 for $60 million in cash

flow! So, we believe that it is a mathematical certainty that if we perform we

will be rewarded over time. The end result is called intrinsic value, defined

as the total amount of cash that can be taken out of a business over its life,

valued in today's dollars. The above example is admittedly superficial and

overly simplistic. However, we have run detailed and sophisticated models and

firmly believe our future is very bright, even using very conservative

assumptions. There is simply no peer company of any size large or small that

comes anywhere close to our cash flow performance. If you want proof, I

recommend you spend the money to come to our meeting for interested shareholders

and investors in Omaha, Nebraska on May 2. At this meeting we will go through

the detailed models and attempt to compare relative valuations over time between

our model and a traditional model.

SEE YOU IN OMAHA. As mentioned above we will hold a meeting for interested

shareholders and investors in Omaha, Nebraska on May 2, two days after our

normal annual shareholders meeting in Waterbury, Connecticut. In addition we

will hold a four day leadership meeting in Omaha at the same time. One hundred

of our top managers from around the world purchased a $2,000+ share of Berkshire

Hathaway this year in order to attend the meeting. We will attend the Berkshire

meeting en masse and then spend a couple of additional days discussing value

creation. As much as I respect Mr. Buffett and believe in the "Berkshire

Principles", the reason we feel so compatible is due to the MacDermid heritage,

most of which was established by my father Harold Leever 50 years ago. If these

principles seem familiar, it's because they are the foundation of MacDermid.

So go ahead and check out the annual reports, the letter to shareholders of MacDermid going back. They are really well-written.

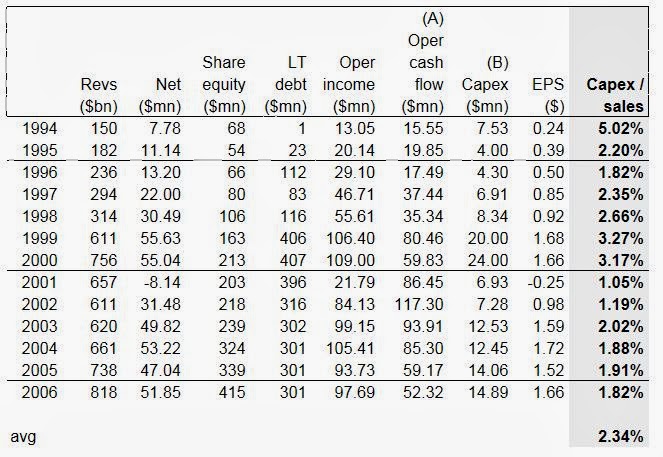

A Look at Some Historical Figures

The key here that grabbed my attention was the high cash flow generating ability of MacDermid. 90% or more of EBITDA becomes free cash flow to them which is very high compared to other specialty chemicals (see above table). Also, their capex is less than 2% of sales. I was wondering if this is sustainable, or if it is just starving needed capex. You never really know in these situations. Sometimes companies will dress things up for a sale or IPO.

So I jotted down some figures from the old filings to see what these figures looked like in the past. Instead of EBITDA, I just used operating income plus depreciation and amortization (OIBDA) because there was less math to do. The ROE figure below is what I calculated using beginning and ending shareholders equity so it won't be exactly the same as what MacDermid reported (ROE wasn't always reported so I decided to use my calculation for consistency through time).

What Leever calls owner earnings in the annual reports is cash flow from operations minus net capex with adjustments for working capital changes, but in my table it's just cash flow from operations minus gross capex. This (owner earnings) wasn't reported consistently throughout the period so I just use my calculation throughout for consistency.

Also, in the recent presentation, they use adjusted EBITDA. None of my figures below are adjusted. The EPS figures are adjusted for a split so is consistent throughout the period.

I split the table in two so you don't have to use a magnifying glass to read it:

MacDermid Financials 1994 - 2006

During this period, sales grew +15.2%/year, net earnings +17%/year, shareholders equity +16.3% and EPS grew +17.4%/year. But you will notice that a lot of the growth came in the period up to 2000.

One of the key measures we are interested in, capex as a percentage of sales, has in fact been pretty low even going back. The average for the 1994 - 2006 period is 2.3%, and since 2001 it has been conisistently under 2.0%. I suppose one can argue that capex was higher when they were growing more pre-2000, but I think a lot of that has to do with the problems they faced in the economy in 2001/2002, restructuring and things like that; they have been recovering since then.

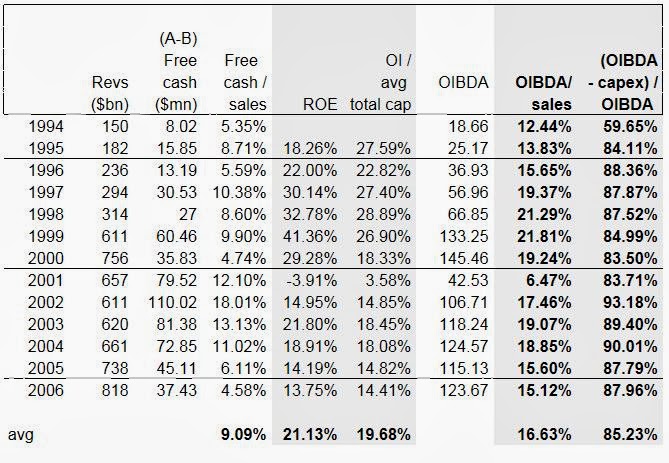

Here is some more detail:

Free Cash Generation 1994 - 2006

First of all, we notice that ROE is pretty decent averaging 21% throughout the period. But again, the period up to 2000 is clearly much higher than post 2000. The OI / avg total cap figure is my proxy for return on capital; it's operating income divided by average shareholders equity plus long term debt. It's a pretax figure, and it shows decent returns.

OIBDA is my EBITDA proxy (less math since it's easier to add operating income, depreciation and amortization than to add earnings, taxes, interest expense, depreciation and amortization). It seems OIBDA margins were pretty good but are now much higher (EBITDA margins above 20% from the recent presentation).

The column all the way to the right shows my proxy for the cash conversion ratio. Again, my figure is different than what they use (OIBDA versus EBITDA, gross capex versus net capex, net working capital adjustments not included in my calculations etc).

But it does show their cash conversion over the whole period is 85% which is pretty high. Even during the period of higher growth, returns and margins (before 2000), cash conversion was above 80%.

So it does look like this high free cash flow generative model is sustainable and is not a case of starving capex for the short term.

Conclusion

This post may be jumping the gun a bit since there hasn't even been a filing for the NYSE listing. I'm sure there will be more detail we need to look at before deciding if this is an interesting investment. I would love to know the final capital structure and ownership details (would love to see if Leever still owns a lot; I know he will roll over his current equity ownership into the new PSP).

But so far this is very interesting to me as:

- Management does seem to be outsider CEO-like and even founder/CEO-like as a substantial portion of his net worth was invested in the company. The current CEO, Daniel Leever's father ran the business for decades so it's sort of a family business in that sense too. The annual reports are great.

- The high free cash flow generative ability and the fact that this model has been sustained over time is very interesting.

- This is not a "a bunch of successful rich guys are involved in this so it should work" kind of investment idea, even though that was the catalyst to make me take a look at this. I wouldn't invest in this just on the reputation of the backers. But it is obviously a positive factor.

- So this is like a compound option (a call option on a call option? Don't ask); you have an outsider CEO (Franklin) buying a company run by another outsider CEO (Leever) backed by a very good stock picker (Ackman).

There are many questions to be resolved, obviously. I guess the biggest one would be Daniel Leever and his plan for the future. He is 65 years old now; his father worked until he was 83 years old (but remained Chairman Emeritus) so there is still plenty of room. But in annual reports in the past he did seem to mention the lack of bench depth. I wonder what the situation is now in terms of succession plans. I also wonder if Leever still has most of his wealth tied up in MacDermid.

Leever has said in the past that their goal was to grow per share intrinsic value at 25%/year. They have come nowhere close to that, which is OK. It's better to have a high goal and do OK rather than to try too hard to make the goal and blow up AIG-like. It seems like the growth plans were thrown off with the recession back in the early 2000s, and obviously the MBO was very poorly timed happening in early 2007 right before capitalism jumped off the cliff.

In any case, I have found enough here of interest to "start a file" on it.

Great post! Man, between this and Colfax, I am 2-2 on suggested entries!

ReplyDeleteYes, thanks for that. Keep them coming. I like how one idea leads to the next and that to another etc... This is the way it's supposed to work; pulling a thread to see where it goes...

DeleteOf all of the Outsider type companies you are looking at, which ones do you think are most like the ones in the book?

ReplyDeleteThat's a good question. A lot of these names are new to me so my thoughts on them are not 'seasoned', but they all look pretty interesting to me. Which is most outsider-like? POST is actually run by an outsider so that looks really interesting to me. And Transdigm is also an outsider company that is still run by the same CEO.

DeleteHmm... So I am having trouble answering this one. There are a lot of other companies that I posted about in the past that are very outsider-ish too, like L, MKL, LUK etc.

So even though it's a good question, nothing is popping into my head at the moment as to which one seems the most 'outsider'-ish... (they all seem to be outsider).

Sorry for the non-answer...

Good initial writeup. It's always a positive for people to quote Buffett and follow a similar philosophy. Plus, the fact they've actually gone to Omaha to meet with and attract similarly-minded shareholders speaks volumes. This is what Markel has been doing for at least a decade and it's how they've attracted such a great, stable base of shareholders.

ReplyDeleteOne problem with the chemical industry I've found is that a lot of companies seem to label what they do as "special" which makes it hard to figure out which ones are truly doing specialty stuff as opposed to commodity type stuff. In regards to PSP in particular, despite having a lot of excellent people associated with it, for some reason they have Stan O'Neal (the idiot CEO who nearly ran Merrill Lynch into the ground) joining the BoD. All I can ask is what's up with that?

Hi,

DeleteYes, Markel is a great Buffett-type company. I love how they have all of their annual reports going back to 1986 (or whenever it was) on their website.

And yes about the chemical industry. What's "special"? I guess it's kind of like insurance. Specialty insurance also has high margins. We can only trust management (what they tell us) and then see for ourself in the numbers. Commodity businesses will have lower margins and maybe more volatile revenues. Commodity business companies will typically make money in boom times and lose money in bad times etc... So looking back at how a company has done usually gives us a hint about how 'special' their products are.

And yes, Stan Oneal on the board was a bit of a shock. I think there are a few toxic names that boards should avoid, but who knows. Maybe there is something there that we don't know about, lol... Let's hope so.

You know, on every investment, the more you dig, you will find *something* at some point...

Thanks for reading.

KK -- if you are looking for more chemical companies that fit the Outsiders template, check out the companies controlled by the Gottwald family of Virginia. Their main public vehicles today are TG, ALB and NEU. The corporate history goes back decades to when Ethyl Corp. was created by GM to manufacture tetra-ethyl lead, and today's companies are the successor spin-outs of that company. --AFR

ReplyDeleteHi,

DeleteI'm not looking for anything in any specific sectors, but I am interested in anyone that fit the outsider CEO model for sure. Thanks for the tips; I will take a look at them.

Would like to suggest to compare PAH to Taminco. Taminco is also a specialty chemical company. It seems to have similar financial traits with PAH - 90% fcf to adjusted ebitda although ebitda margin is in the low-20s. Not sure about the quality of the CEO though, unlikely to be an outsider.

ReplyDeleteThanks for the tip! Always worth a look, or at the very least a quick look.

DeleteWould also like to suggest another company though has nothing to do with chemical. But I think it may interest you because personally, I think the management is an "outsider" and the annual letter written is of the highest standard. It is Credit Acceptance Corporation. The current CEO is a young chap (late 40s) with a long runway ahead of him. Although young, he has been the CEO since Jan 2002, and under his charge, CACC is up almost 1300% versus S&P of 55% - an outperformance of over 23x better.

DeleteThanks for the CACC idea. I will check it out. I think I've looked at it before a while ago but not recently.

DeleteThanks again for a great post KK. Sorry my comment here is a bit off topic... I find your post on SPE also very interesting (too bad I didn't know about your blog back when you had the original post). What are your thoughts on management of SPE also running a hedge fund? It seems they might be more incentivized to boost returns on the hedge fund vs SPE. In the less liquid world of CEF if they do all the trades on the hedge fund first it would not be helpful for the SPE investors, don't you think? I was about invest in SPE until I thought about this point.

ReplyDeleteBack to the PLAHF, it is trading at $12 OTC. Since there are no filings, and we know nothing about the capital structure, how do you think the market arrived at this value?

Hi, that's a good point. But if you go back and read about Goldstein, watch video interviews etc... he does not look like the guy that would play games like that (take advantage of publicly listed entity to benefit hedge fund). So I wouldn't worry about that at all.

DeleteAs for PLAHF, I have no idea what that price represents. I don't know if the stock even trades at that price, or if it's just a place-holder-like price that someone input for now but with no bid/ask.

What do you think of Fairfax Fiancial Holdings( Markel has a material holding in them)? The valuation seems much more cheaper than Markel. Fairfax's positions in Blackberry, equity hedge and deflation hedge make it unpopular with investors now. But is it temporary? Is Prem Watsa an outsider CEO? Thanks for another informative post.

ReplyDeleteHi, I like Watsa and Fairfax. I have written about it in the past here; maybe it was just a comment on his CPI trade.

DeleteI tend not to like his hedging out the equity exposure, but his returns in the annual report show returns including equity hedges and on that basis the long term performance is still really good. So maybe it's not an issue. It is an insurance company and he is investing float, and the default investment is usually bonds, so I guess on that basis, he is not out on a limb too much.

As for his CPI trade, I see that as a low cost trade; if it doesn't work out it doesn't cost him too much. The trade is not going to blow up FRFHF by any means at all. He just loses the premium paid, which is small compared to the total portfolio. So think about that as embedding some optionality in the portfolio in case Japan-like deflation spirals out of control. You never know. He points to his being early on subprime too.

Blackberry is pretty ugly, but that's just one investment. People do tend to look at one or two trades and try to make judgements about someone with that. I guess that's availability bias or recency bias or whatever. But it's not a big part of the portfolio, so the attention is overdone, I think. This is sort of true with Ackman too; sure JCP and HLF are disasters (well, HLF isn't over yet), but over time Ackman has a great track record. I wouldn't jump to any conclusions based on these two investments.

FFH is an interesting case. Prem Watsa seems to be one heck of a smart guy and his annual reports are definitly worth reading (if you are as nerdy as I am). What I don't like though is the combined ratio. It remains pretty stubbornly above 100 across all entities, even if some show lower combined ratios. So his float is not really free. It is cheaper than Canadian govie paper that but that is not the point imo. MKL does a better job here with a combined ratio below 100 about two in three years.

DeleteLove the Outsider theme, read book over Thanksgiving great read. Have you read the paper on Buffett Alpha from Yale talking about leverage and Sharpe ratio of BRK?

ReplyDeleteHi,

DeleteNo, I've heard about it but haven't read it.

Thanks for reading.

PLAHF is traded as "Grey Market", from the OTC website:

ReplyDeleteGrey Market

There are no broker-dealers quoting this security. It is not listed, traded or quoted on any U.S. stock exchange or on any of the OTCQX, OTCQB or OTC Pink marketplaces. Trades in grey market stocks are reported by broker-dealers to their Self Regulatory Organization (SRO) and the SRO distributes the trade data to market data vendors and financial websites so investors can track price and volume. Since grey market securities are not traded or quoted on an exchange or inter-dealer quotation system, investor's bids and offers are not collected in a central spot so market transparency is diminished and Best Execution of orders is difficult.

KK, hope you had a happy holiday season and New Years. We look forward to your next blog post.

ReplyDeleteThanks,

DeleteI had a good holiday season. I realize I haven't posted in a month. December was a bit busy with some travelling (fun stuff), holiday business etc...

But stay tuned. I'm still here and will be posting a bunch this year.

Any word on when Platform Specialty Products will be listed?

ReplyDeleteI have no idea. I'm wondering about that too.

DeletePlatform Specialty Products, PAH, is expected to list its shares on the New York Stock Exchange on 1/23/2014

Deletehttp://online.wsj.com/article/PR-CO-20140122-911438.html

Thanks!

DeleteTBI,

ReplyDeleteBAC, WFC, GS and JPM results are out by now, any updated thoughts on the banks, especially on JPM?

To me it seems that everything has been rolling on as expected which is surprising by itself in a way... WFC is WFC, JPM had their show, BAC cut expenses.. I did expect GS to get a bit more aggressive but obviously that was wrong.

Thanks!

HI,

DeleteNot much new. I still like them but not as much as when I first started posting about them in late 2011 when Occupy Wall Street was in the news every day. Now they seem to be well-liked and seems to be a favorite sector for many, so obviously it's not so exciting.

Business-wise, they are all doing great, but there is still the issue of revenue growth. If revenues don't grow and the economy starts to turn, then that would be awful because credit costs will rise and there will be no growth to offset the decline in earnings. That is not my expectation, but it is a risk.

I don't worry too much about capital and regulations. Dimon said that the analysis on wall street that show that banks will have lower returns due to higher capital requirements and Volcker rule are doing a static analysis, an 'all else equal' sort of analysis but aren't really thinking about how banks will reprice, readjust their models etc...

And I believe that is true too. Banks are living, dynamic entities so they will adapt and will make money.

As for GS, I agree. I believed Viniar all this time saying that their low ROE was basically their choice of waiting for opportunities (rather than rushing to repurchase shares and then needing capital later when opportunities arise). But it's been a long time and their ROE is subpar. The economy is doing fine and the stock market was up 30%. So it's not like the environment is bad.

I still like GS, of course, but I think maybe something has to happen there...

KK,

ReplyDeleteBecause this started as a SPAC, this issue comes with warrants. Warrants offer additional leverage as opposed to common stock. what is your opinion on the outstanding warrants?

Are the warrants listed? If so, under what symbol ISIN? Thx

DeleteHi,

DeleteThe warrants were listed in London before trading was halted (to switch listing). The S4 said that they expect the warrants to trade on the OTC market, but I don't see it listed in any search.

Hi,

ReplyDeletewhat's your take on the dilusion?

Currently there are 103,576,300 ordinary shares outstanding.

Total diluted shares would be 132,913,266 (401(k) conversion + warrants + Founder Shares conversion + exchange shares + option exercises) which is almost 30% dilution.

This does not include the special dividends paid in common stock to the Series A Preferred Stock holders. When the stock price exceeds $11.50 for last 10 days of calendar year, founder preferred shareholders receive a dividend paid in ordinary shares in the amount of 20% over the IPO price of $10. In subsequent years the dividend is based on the highest Dividend Price previously used. Life of the shares can be extended for 3 years at the request of the Founder Entities and the Board. Currently there are 2,000,000 founder shares outstanding.

Also: "We are currently authorized to issue an unlimited number of no par value shares which may be either ordinary shares or preferred

shares." (p.3)

Thanks

Well, it's quite dilutive. There will be a lot of cash coming in, though, like for the warrants. And the founders share 20% payout is their way of setting up the private equity-like 'carry' so it's expensive, but no worse than if you owned a private equity fund that owned one business.

DeleteI don't own it yet as I would like to see it trade a little and have it go through some earnings reporting cycles to see what the post-deal business looks like...

Thanks for the fast reply. Just calculated that the Series A dilution would be 0.2% if the stock price reaches $20. So not a big deal as far as I'm concerned.

DeleteActually, 0.2% sounds a little low. How did you calculate that? You know the series A preferreds receive 20% upside, but the payout is based on A x B where A is the price appreciation above something and then B is actually the number of ordinary shares outstanding as of May 2013, plus the conversion of the preferreds. So they are taking 20% of the upside that ALL (or most) of the shareholders are getting, not just the 2 mn preferreds. I may be reading this wrong, but that's my take, so it's much more onerous than you might think.

DeleteBut then again, even still, that's no different than a typical private equity fund so not a deal-killer on its own.

i tried reading the prospectus and the faq on the homepage, but couldn't make any sense of this. never come across something like it before. i know you probably don't take requests but if you get it would be a huge service to us possible investors if this dilutive effect was broken down somewhere. sorry in advance!

DeleteHi, it's on page 112 of the S4 filed in January. I may be reading it wrong, but here is a cut and paste (in pieces due to size limit of comments):

DeleteSeries A Preferred Stock. Prior to the Domestication, Platform had 2,000,000 Founder Preferred Shares outstanding. In connection with the Domestication, each Founder Preferred Share will be converted into one share of Series A Preferred Stock of Platform Delaware. The special rights, preferences and privileges of the Series A Preferred Stock are set forth in the form of the new certificate of incorporation attached to this prospectus.

Dividends. Subject to applicable law and the rights, if any, of any series of preferred stock of Platform Delaware ranking senior to the Series A Preferred Stock as to dividends, at any time subsequent to the consummation of the MacDermid Holdings Acquisition, if the average closing price per share of common stock is $11.50 (subject to adjustment in accordance with the certificate of incorporation) or more for ten consecutive trading days, the holders of the Series A Preferred Stock will be entitled to receive, in respect of each calendar year (or period commencing on November 1, 2013 and ending on December 31, 2013) (each a “Dividend Year”), a cumulative annual dividend amount (the “Annual Dividend Amount”), which is calculated as follows:

cont'd:

DeleteSeries A Preferred Stock. Prior to the Domestication, Platform had 2,000,000 Founder Preferred Shares outstanding. In connection with the Domestication, each Founder Preferred Share will be converted into one share of Series A Preferred Stock of Platform Delaware. The special rights, preferences and privileges of the Series A Preferred Stock are set forth in the form of the new certificate of incorporation attached to this prospectus.

Dividends. Subject to applicable law and the rights, if any, of any series of preferred stock of Platform Delaware ranking senior to the Series A Preferred Stock as to dividends, at any time subsequent to the consummation of the MacDermid Holdings Acquisition, if the average closing price per share of common stock is $11.50 (subject to adjustment in accordance with the certificate of incorporation) or more for ten consecutive trading days, the holders of the Series A Preferred Stock will be entitled to receive, in respect of each calendar year (or period commencing on November 1, 2013 and ending on December 31, 2013) (each a “Dividend Year”), a cumulative annual dividend amount (the “Annual Dividend Amount”), which is calculated as follows:

A X B, where:

A = an amount equal to 20% of the increase (if any) in the value of a share of Platform Delaware common stock, such increase calculated as being the difference between (i) the Average Price (as defined in the Platform Delaware certificate of incorporation) per share of Platform Delaware common stock or Platform ordinary shares, as the case may be, over the last ten days of the relevant calendar year for such annual dividend (the “Dividend Price”) and (ii) (x) if no Annual Dividend Amount has previously been paid, a price of $10.00 per share of Platform Delaware common stock, or (y) if an Annual Dividend Amount has previously been paid, the highest Dividend Price for any prior Dividend Year (provided in each case such amount is subject to such adjustment either as the Board of Directors in its absolute discretion determine to be fair and reasonable in the event of a subdivision, combination or similar reclassification or recapitalization of the outstanding Platform Delaware common stock or otherwise as determined in accordance with the certificate of incorporation, in each case without a corresponding subdivision, combination or similar reclassification or recapitalization of the outstanding shares of Series A Preferred Stock); and

B = a number of shares of Platform Delaware common stock equal to such number of shares of Platform ordinary shares as was in issue on May 17, 2013 plus the number of Platform ordinary shares issuable upon automatic conversion of the Founder Preferred Shares in accordance with the Platform BVI Articles (as defined below) of Platform BVI as if converted on May 17, 2013, which such amount is subject to such adjustment either as the Board of Directors in its absolute discretion determine to be fair and reasonable in the event of a subdivision, combination or similar reclassification or recapitalization of the outstanding Platform Delaware common stock or otherwise as determined in accordance with the certificate of incorporation, in each case without a corresponding subdivision, combination or similar reclassification or recapitalization of the outstanding shares of Series A Preferred Stock.

Each Annual Dividend Amount shall be divided between the holders pro rata to the number of Series A Preferred Stock held by them on the relevant Dividend Date (as defined in the Platform Delaware certificate of incorporation). The Annual Dividend Amount will be paid no later than ten trading days from the Dividend Date by the issue to each holder of Series A Preferred Stock of such number of shares of common stock as is equal to the pro rata amount of the Annual Dividend Amount to which they are entitled divided by the average closing price per share of Platform Delaware common stock on the relevant Dividend Date.

thanks a bunch! so in simplified math if the stock goes to 20 at the end of the year, the holders of the preferreds get 200 million usd in stock. this would be around 10% of market cap then. do you know how long these prefs are around for? the prospectus said their life can be extended to 3 years total by board. i hope this means they get one dividend and when they do then that's it. the board could extend the life if they (for example because of a market correction) don't get their extra stock. that's what i HOPE.

Deletethe worst case scenario is that the board could just decide every 3 years they still want to dilute the common stock holders and the stock dividends would continue to infinity. but that just sounds so wrong and i wouldn't like to believe that of the people running this. they would have to beat the market by 25% every year just to break even.

nobody take this too seriously as i'm just typing out my thoughts without fully understanding the subject. would really appreciate different views on the subject.

I don't know how long it will actually last, but this is no different than your typical private equity fund and carried interest. Private equity guys take 20% of realized profits; that goes to the general partner, so this preferred interest is sort of like a general partnership interest. Hedge funds also take 20% of the profits as incentive fees.

DeleteI don't think they need to make 25% to break even. If the stock price goes up just a little bit, then 20% of that is small, so there is not much dilution. They also have a high watermark provision built in. I think they only get paid on appreciation above the previous highest dividend price (or whatever they call the price at which they calculate the dividend); so if the stock goes to $20/share and they pay a dividend in year one and then the stock goes back down to $10, they can't get paid on a rally back up to $20 again the following year. The following year, the stock price would have to be above $20 for them to get paid.

So just think of it as a private equity fund, except they get paid on stock price appreciation whereas private equity funds get paid on realized profits.

Anyway, it is a layer of cost that you have to take into consideration when comparing this to other specialty chemical companies.

Do you know much about Mariposa Acquisition LLC, now the second largest shareholder behind Pershing Square?

ReplyDeleteActually it must be Martin Franklin's vehicle...

Delete>John Griffin's hedge fund firm Blue Ridge Capital has filed a 13G with the SEC and disclosed a position in Platform Specialty Products (PAH). Per the filing, Blue Ridge now owns 7.72% of the company with 8 million shares.

ReplyDeletehttp://www.marketfolly.com/2014/02/blue-ridge-capital-discloses-platform.html?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+MarketFolly+%28Market+Folly%29

My worry is with how the preferred shares are set up, whether the management's interest is aligned with that of shareholders. I guess Griffin is OK with it, after all he runs a hedge fund.

Thanks for the update. That is very interesting. The concern with these SPACs is that the founders may just want to play for the post-acquisition 'pop'; when a SPAC acquires a company, the SPAC gets revalued as an operating entity often at a price much higher than initial book value (arbitrage between private business valuation and public market valuation). So some SPACs might be good for the pop but not much afterwards.

DeleteBut in this case, since there is that preferred share incentive (20% of upside), the founders do have an incentive to play for more than just the pop, but increased value going forward.

In this sense, the 20% incentive may be worth it; it's no different than a private equity fund (not exactly, but just broadly speaking). If the founders can be an extra antenna and can be instrumental in finding future acquisitions for Platform above and beyond what MacDermid could do by itself, then the incentive may be well worth it.

In any case, if Blue Ridge is coming in after the MacDermid acquisition, NYSE relisting and valuation pop, that is very interesting.

KK,

DeleteAt stock price of $14.43, what is the EV of PAH?

I can't find its S-1. The IPO is pretty confusing to me.

Hi,

DeleteThe S-4 is here: http://www.sec.gov/Archives/edgar/data/1590714/000119312514014628/d622226ds4a.htm

Yes, it's quite messy. But you can use something like 130 million shares, I think. That's the diluted shares used for the proforma 9 months through September. That is close to what you get when you add up post-offering 106 million shares with the other dilutive stuff; options, warrants and PDH shares exchangable to ordinaries. Debt is $741 million. There is some other liabilities like deferred taxes and present value of payouts to equity holders of MacDermid (up to $110 million or something).

I haven't gone through this in detail as I am hoping for year-end figures to come out soon.

Oops, forgot to mention; if you use the diluted shares without adjusting for cash, it will be conservative. When warrants and options are exercised, cash comes in the door; for example when $10 strike options are excercised on a million shares, $10 million comes in the door and cash is of course reduces EV.

DeleteKK, have you gone through PAH's 10K? If so, what are your thoughts?

ReplyDeleteHi,

DeleteYes, not in too much detail. My thought is, it's a mess! But that doesn't mean it's bad. They did another acquisition so I guess we have to see how things evolve going forward as things normalize on the financials (if they ever do).

Ackman talked about PAH during the VRX/AGN presentation; something about the value of a platform etc.

Pg 84 of the link is where Ackman begins to talk about "platform value": http://vpsevent.com/wp-content/uploads/2014/04/The-Outsider-Presentation-4.22.2014.pdf

DeleteKK - what were your thoughts re: PAH's equity follow on and the large stock price run up prior to that?

ReplyDeleteI don't have any particular thought or insight into that. Are you suggesting something suspicious (someone ramping the stock so they can raise equity)?

DeleteAs for raising equity, obviously it's the best when a company can grow without issuing equity, but when the stock price rises a lot it's not a bad idea to issue shares to raise capital. Of course, this is not the BRK way, but other outsider-type CEOs do so. POST did it recently and LMCA did it last year too (via a convertible).

And why did it rally so much since May? I don't know. My guess is that the story is getting out. Before, it was sort of ignored as just another SPAC / blind trust but it seems like they made a really good acquisition. And the latest acquisition looks good too. Leever sounded totally ecstatic on that conference call, you can literally *hear* the feathers sticking out of his mouth.

I guess the attention to Ackman has raised the visibility of it too. Last year, Ackman was a total loser (JCP, HLF etc...) and now he is a star again. And he talked about PAH during the VRX/AGN meeting too, talking about how this is a platform opportunity etc...

Interested to hear if you have any thoughts on Nomad Holdings? http://www.nomadholdingslimited.com/uploads/Haddock%20Lender%20Presentation.PDF

ReplyDeleteHi, it sounds pretty interesting. I can't get a handle on what kind of business they bought as I am in the U.S. I'm not too familiar with Gottesman.

DeleteJust curious if you've looked at PAH lately. THe stock price has gotten crushed, down over 40% just in 2016 and 50% below the IPO price. I guess the market is starting to get a little worried about the companies debt level. Its 2022 bonds are trading at 82 cents on the dollar, priced to yield 8%. Given the selloff in junk, I guess the yield seems about right but does indicate some worry about the debt. I haven't done enough research yet to have a strong opinion, but seems like this could be a pretty good speculation if you believe the debt is manageable things won't get much worse. At the current enterprise value, the market values the company at a significant discount to what it previously paid for all its acquisitions, including MacDermid.

ReplyDeleteHi, PAH is interesting. It's getting hit, I think, for many reasons so is pretty interesting, I think. For one, after VLX, the market started to frown on these acquisition-based businesses. That was a double whammy last year when VLX took a hit; PAH was also a serial acquirer and also was owned by Ackman (so was easy target to front-run redemptions etc...). Then the junk bond market fell apart so that was another kick to these roll-up type stocks. And then of course the oil market tanking even more and China falling apart really took the industrials down hard.

DeleteSo we will have to see how much the businesses of PAH are getting hit. If it's not so bad, then it's a great buy down here.

A positive is that Jarden was sold and Martin Franklin said that he will spend more time now on PAH.

BI, I hope you are doing well. Have you spent any time on PAH lately? I've spent some time digging and think the stock is extremely cheap. Fears over excessive leverage are overblown and the company has the capacity to tap its lines of credit to pay off the Permira preferred stock liability in October if necessary. With no significant debt maturities until 2020, the company has time to delever. Even without a recovery in end markets, the interest expense is manageable and the company will likely produce nice free cash flow. I think based on 2016 guidance and the fact that the dollar now seems to have stopped appreciating, fcf could be over $150 million in 2016. I'm really liking the upside here with the stock below $9.Do you have any thoughts? Thanks.

DeleteOops, sorry. I try to respond to stuff; must have forgotten as I remember reading this comment.