BRK now owns more than 35 million shares. The most recent buy occurred between $53 - $56/share. The stock is now trading at over $58, so that's a $2 billion position.

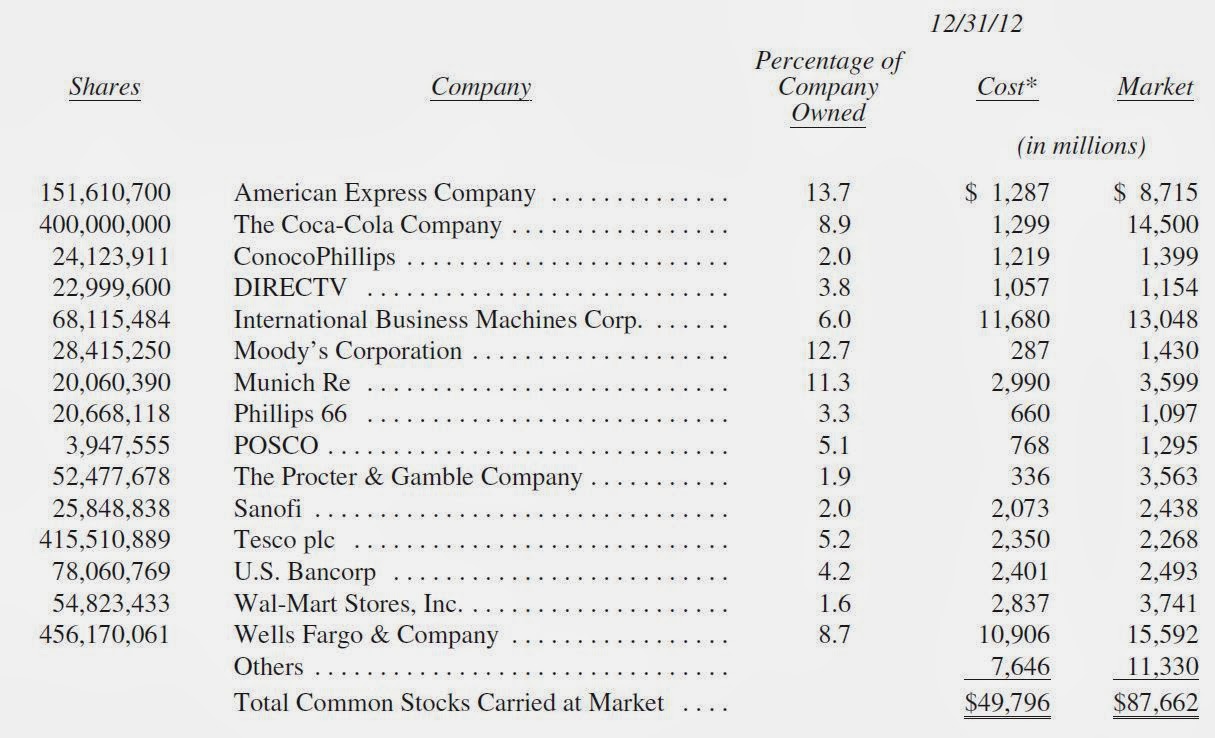

The BRK annual report includes stock holdings with a value of more than $1 billion, so this DVA position will make it into the 2013 annual report. Just out of curiosity, here's a look at the December 2012 stock holdings:

Stock Holdings of Over $1 Billion

As of December 2012, DTV was the only pick on the list from the new managers (and this one is a Weschler pick too). The market is up quite a lot and there have been major purchases so this list will look a little different at year end, but it still shows you how big this DVA investment is, relative to BRK, even though it's only 2% or so of the equity portfolio (which was fair valued at $105 billion at the end of the 3Q 2013).

Also quite interesting is that Ted Weschler himself, his daughter and some trusts that he runs own a big position in DVA. In the November 12 filing, it shows that Weschler has a 2.2 million direct ownership stake in DVA, which comes to $130 million. That's a pretty big position.

I looked at this before when Buffett hired Weschler (and everyone started dissecting his hedge fund holdings) and I didn't think much of it. I thought, "different strokes for different folks". I've looked at dialysis center stocks before and remembered their stocks tanking on Medicare payment cuts (or threats). The common view (ever since at least the late 1990s) was that this is a business that can be destroyed by a single stroke of the pen in Washington DC. Why invest in a business that an irrational congress can blow up so easily?

I still held this view when I looked at DVA recently. But this recent purchase made me scratch my head so I decided to dig a little deeper to see what's going on here. Weschler is not a reckless gambler/risk-taker. He is a very rational investor. So whatever he is doing, he is certainly not betting on the outcome of the impact of the ATRA 2012 (see excerpt below on the American Taxpater Relief Act of 2012), Affordable Care Act and many other factors (you can read a bunch of risk factors in their 10-Qs and 10-Ks).

Going forward, obviously, Weschler's and Comb's picks will be more interesting to follow than Buffett's (who is limited to looking at only the 50 - 100 largest cap names). So this is something we Buffett followers have to do: study Ted and Todd's hopefully excellent adventures.

Here's one of the big issues people are worried about that will take effect in 2014 (CMS is Centers for Medicare and Medicaid Services):

Risk that our rates are reduced by CMS. The American Taxpayer Relief Act of 2012 mandates that the Secretary of Health and Human Services (HHS) reduce dialysis payments beginning in January 2014 to reflect the Secretary’s estimate of changes in patient utilization data from 2007 to 2012 for erythropoiesis stimulating agents (ESAs), other drugs and biologicals that would have been paid for separately under the composite rate system, and laboratory services that would have been paid for separately under the composite rate system. The Secretary must also use the most recently available data on average sales prices and changes in prices for drugs and biologicals reflected in the ESRD market basket percentage increase factor. CMS has asked for comment regarding phasing in any reduction over a one year or longer period. In the proposed 2014 ESRD PPS rule published on July 8, 2013, CMS determined that the ESRD Prospective Payment System (PPS) base rate that otherwise would apply in 2014 (inclusive of the market basket update of 2.5%) should be reduced to account for reductions in the use of drugs and biologicals between 2007 and 2012. This cut represents a significant reduction (inclusive of the market basket update of 2.5%) of 9.4% in Medicare payments that is proposed to take effect January 1, 2014 for calendar year 2014. Although the proposed rule is not final, if it is implemented as proposed, it could have a materially adverse effect on our business and financial condition. Any reduction in dialysis payments will negatively impact our revenues, earnings and cash flows.

So Why DVA?

I'm not going to do a thorough analysis of DVA here. I just wanted to make some major points that I realized as I took a look at this thing. And then I realized that DVA has components of two themes that I talk about here.

First of all, let's see how DVA has done over time. The current CEO, Kent Thiry, became CEO in October 1999. DVA (previously called Total Renal Care Holdings) at the time was in bad shape; probably due to bad acquisitions/big merger, too much debt and bad execution. He really turned the company around.

Here is the chart of DVA since Thiry took over:

DVA Since October 1999

The red line is the S&P 500 index and the green line is BRK.

DVA has returned +25%/year since October 1999 versus +2.0%/year for the S&P 500 index (excluding dividends) and +7.3%/year for BRK.

Here's a more recent look; the last five years:

DVA Last Five Years

Free Cash Flow

(figures adjusted for 2013 stock split)

The first nine months of 2013 has also been pretty decent, and cash flow and free cash flow for the last twelve months through September 2013 was $1.62 billion and $1.24 billion respectively. Using the 9 month average shares outstanding of 215 million shares (close enough), that comes to $5.77 in free cash per share generated in the last twelve months. With a stock price of $58/share, that's 10x free cash.

That's pretty cheap. But of course, it's not so simple. Thiry did say that 3Q 2013 was exceptionally strong. And these numbers, although they reflect sequestration, don't reflect the problem shown above that kicks in in 2014, not to mention the substantially lower earnings expected from HCP that they mentioned.

We know that DVA has done incredibly well in the past, but how can we get comfortable (or how does Weschler get comfortable) about DVA going forward? That's the big question. Even though there are a lot of trends in favor of DVA (increasing obesity / diabetic rates, demographic trends (including racial composition of population) favor increasing rates of diabetes etc), there are trends that don't, like government funding problems (medicare / medicaid = bust), Affordable Care Act and other cost pressures on health care in general etc.

Howard Mark's Second Level Thinking

So here is where it gets interesting. I have been guilty of "first level thinking" on this issue for at least a decade. The first level thinker of DVA thinks it's a bad idea because their biggest payor is the U.S. government which is broke (and broken). If pricing and terms can be set and reset at the whim of congress, who wants to be on the other side of that? DVA and other health care providers have faced this issue for years. Private health insurers too, will be a source of increasing pricing pressure (as was discussed in the 3Q conference call). ACA may make that worse as private health insurers have to lower cost too.

But first, a detour to another situation this reminded me of:

Warren Buffett's Second Level Thinking on Banks

After the crisis, people wondered why Buffett kept investing in banks; isn't the golden age of banking over? Won't new regulations and lower leverage make banking a low return business? Won't the return on equity of banks going forward be really low? With interest spreads shrinking, how will banks make money? Won't Wells Fargo, one of the biggest, be the hurt most from these trends?

Buffett's response was simple. He said that in any industry, the one with the lowest cost wins. No matter what happens in the economy, if you have the lowest cost, you will win. This is true in any industry.

His point was that all of these negative trends will hurt all banks equally, but if you have the lowest cost, it will hurt you the least. The high cost players will be run out of business, and the lowest cost player can probably pick up market share. This is how it has always been in any industry.

This is precisely what seems to be happening in the banking industry now, with market share increasing at Wells Fargo (and Bank of America and JP Morgan too).

Back to DVA

So, getting back to DVA. DVA is staring at some serious issues going into 2014. But the key point here is that this is an issue that will face all dialysis (and other healthcare) providers. Drastic payment reductions will put many small operators out of business. DVA seems to be a very efficient operator (high margins) with very good patient outcomes (various metrics are disclosed every year in the annual report).

Without going into too much detail, I think we can assume that DVA is one of the most efficient operators out there.

During the 3Q conference call, analysts couldn't understand how Thiry can price and purchase dialysis businesses without a clear insight into how all of these new health care issues will play out in congress (and elsewhere). And interestingly, he insisted that they don't make purchases or price deals based on short term considerations, but they base it on a view of how things will look six or seven years out (or something to that effect).

The point is that if there are drastic payment reductions, they will simply have to cut costs to accomodate the new structure including closing some centers that don't make economic sense.

And judging from the numerous independent and non-profit operators out there, he feels that many of them won't be able to survive in a scenario of drastic cuts. This would force rationality on the part of the CMS (or else face a lot of problems from patients who may lose access to much needed care when too many centers close).

So basically, the less efficient operators should provide a floor to pricing such that in any scenario, DVA should be able to do well (even though there might be short term reset shocks to revenues / stock price etc.).

If they do insist on cuts even with the negative impact on many other less efficient operations, this may provide an opportunity for DVA to move in with more efficient and possibly profitable operations. Or who knows, this may even lead to a big acquisition by DVA (to take a big bite of market share).

Either way, the view must be that over time, say five to seven years, things will settle down to a level of stability and due to DVA's strong competitive position of efficiency and positive patient outcomes, they should come out the other end stronger. They will be a beneficiary of that (even though I would guess that Thiry would rather not have such a big shock to the system).

Outsider CEO-like

And not to overplay this idea, there is something sort of outsider CEO-like about Thiry. They grow through acquisitions and focus on capital allocation and free cash flow plus strong execution. Thiry doesn't own a whole lot of stock, which I find curious. So he doesn't quite fit the owner-operator model. Given the stock price performance over the past 14 years, I bet he wishes he held on to more stock too. But who knows what the situation there is.

Conclusion

So, the fact that there is some pricing pressure (including a big change from CMS in 2014) and uncertainty with respect to the ACA and other changes is a concern for any rational investor. But to stop thinking there (single biggest payor = U.S. government = bad investment) is first level thinking.

Thiry believes that DVA offers superior service to other dialysis centers, and that HCP (recently merged, non-dialysis health care business) is part of the solution to the health care cost problem. In this case, when the dust settles they should come out of all of this better off.

I can't imagine a scenario where payments get so low that many operators can no longer survive. Five to ten years from now, there will be a dialysis business and someone will be doing it profitably (or else the industry would disappear and that's not likely to happen).

There is also a sort of time arbitrage factor at work here; many seem focused on the short term outcome of various changes in the health care industry while others like Weschler focus on the long term outcome (superior management / execution will get the business to a better place regardless of what happens as any adversity will be an opportunity to increase market share).

There are other risks, but for this post I just wanted to focus on this aspect of DVA that I find very interesting as it sort of illustrates the concept of first and second level thinking, how the strong operators with competent management may be able to take advantage of adversity, and the importance of capital allocation and free cash flow generation (which makes it possible for strong operators to exploit opportunities as they arise).

Great post. HCA built an incredible business on this same theory. So long as the company could operate at a level of profitability sufficiently above the not-for-profit hospitals, they would have a buffer against draconian CMS cuts. The government cannot have a long-term reimbursement strategy that knocks out a significant portion of hospital beds. Perhaps DVA is the exact same idea.

ReplyDeleteThere is one caveat -- if I recall correctly, HCA collects just north of half of their revenues from Medicare, etc. DVA collects nearly 70% from Medicare if memory serves (and 90% of their patients are Medicare, etc). So, 10% of patients (the commercial payors) are putting up nearly 30% of the revenues. That seems a little more dangerous.

Yes, that's about right. In 2012, 66% of revenues was from the government, and 90% of the patients were on govt plans. 10% of the patients are carrying a lot of the load, and pressure there would be a concern for DVA.

DeleteBut I think the feeling I get from going back and reading about DVA is that they are a preferred provider on both ends. On the one hand, the government can't cut reimbursements so much that it puts everyone else out of business (including many DVA centers that would probably have to close). And on the other hand, the good patient outcomes should be an advantage for private insurance carriers too for their own overall cost etc.

So if both of these are true, then things should stabilize somewhere not too detrimental to DVA. I was going to write more about those issues but decided to keep this post short. There is a lot written about DVA and hopefully DVA itself will reveal more about this sort of thing in the near future. I think there is an analyst day or investor day coming up on December 9, I think it was, where they will talk about the 2014 issues more.

Either way, I think the argument still holds that the low cost, efficient operator is going to walk away in much better shape either way, barring total disaster on both ends (commercial and govt) which I think is unlikely...

also international

ReplyDeleteHi Brooklyn Investor, glad to see that you bascially share my views on Davita which I recently detailled on Seeking Alpha.

ReplyDeleteBringing Fresenius into the picture IMO is key if you really want to understand the industry. Fresenius, being more international, has to deal with dozens of different healthcare systems around the world, which shows that this industry can do well with any healthcare system there is.

Here is my article:

http://seekingalpha.com/article/1769952-why-davita-is-undervalued-compared-to-fresenius-medical-care

Hi, that's a nice analysis. People do worry a lot about payments but I agree it's a highly necessary procedure so I can't imagine payments not settling at some reasonable level over time. It's not like a military contract for a new fighter that can be cancelled outright or anything like that. This is a service that is needed and will be done by someone at a profit (eventually).

DeleteThanks for reading.

kk, thanks again for brk related topics. if you have the time, how much value can buffett add trying to cherry pick with buys like ibm and xom, over just buying spy and going fishing ? WHY does buffett love ibm and xom over buying back brkb ? buffett doesn't take those type of questions, maybe you can opine ? Thanks.

ReplyDeleteBuffett has outperformed even with large blue chip stocks (at least since the 1980s), so it's definitely worth his time. With a $100 billion equity portfolio, even a 1% outperformance is worth $1 billion/year. I think if all else equal, he would rather buy a business than buy back stock. He just loves buying stocks and businesses. I think some of the outsider CEOs might be much more eager to buy back stock to keep their capital structure 'optimal', but Buffett is not into that sort of thing. He wants to be rational, but doesn't have to keep everything 'optimal' at all times. Even when BRK stock is cheap he is eagerly looking for that big elephant and other opportunities including insurance (if the market hardens suddenly, BRK can write a lot of business).

DeleteIf BRK got stupid cheap, I'm sure Buffett would buy back a ton of stock... but I don't think BRK has gotten stupid cheap all that often. That doesn't mean IBM and XOM are stupid cheap; I think he has a higher hurdle for buybacks than buying other businesses but who knows...

I don't really obsess over things like that, like why BRK doesn't pay dividends or buy back stock. Buffett just loves buying stocks and businesses and both of those returning capital to shareholders reduces what he can do.

Of course it will be interesting to see what happens when his returns aren't as good as it was in the past and buybacks start to look more reasonable. I don't think we are there yet, but we might get there some day.

Thanks for reading.

One question on the cash flow/capex discussion. If you're valuing it based on a traditional DCF model, you can't exclude growth capex from the cash flow calculation if you're also modeling top-line growth at a higher rate due to the growth capex. In other words you can't give them the benefit of the growth capex in the top line but not penalize them on the bottom. If you exclude growth capex from the cash flow calc, it's a much lower top-line growth company, which implies a lower valuation all else equal, right?

ReplyDeleteYes, that's right. You can't model growth without including growth capex. This figure just shows you what steady-state free cash would be. The reality is that this free cash is reinvested in the business through opening of new centers and acquisitions at a decent return.

DeleteIf a company owned a 10% yielding bond and it paid out all of this 'free cash' as dividends, then the business wouldn't grow, but it would still be returning 10% every year. That's not bad at all. If they bought more bonds every year wit the 'free cash', then the business would be growing 10%/year even though there would be no 'free cash' returned to shareholders, but that's OK too.

If the return on capital is higher than 10%, then that's all the better even if there is no free cash after growth investment.

But in any case, yes, if you plug in figures for a DCF model then you would have to include growth capex needed to accomodate whatever revenue growth you model.

That makes sense. I was thinking 10x cash flow might sound cheap but may actually be a fair multiple if it reflects a top line that grows only low-single digits organically. But you're saying the ROC matters, such that a business that can invest its next dollar earned at well above its cost of capital should trade higher than 10x even if top-line growth is low. The DCF is agnostic as to returns though, so how to reflect this. Maybe pull out all growth capex in the terminal year since you're using a lower, steady-state growth rate in the terminal value calc anyway? That way, the cash all flows to FCF and is included in the valuation.

DeleteYou can do that, but I don't usually spend too much time on terminal value and things like that. If a stock is trading at 10x free cash and you know that management will use that capital wisely to increase value of the company, that's usually good enough for me.

DeleteIf you really start to dig into this company, it doesn't really seem like a Warren Buffett stock.

ReplyDeleteThere are reasons why the various settlements DaVita has paid are so large. They have been doing some pretty unethical things. (I think I would make this argument against Goldman Sachs too, which is a deal that should be attributed to Buffett.) DaVita overdosed its patients on EPO so they could split profits with Amgen. They allowed kidney doctors to have stakes in DaVita clinics so that there would be conflicts of interest. These doctors would drive patients towards their clinics, even if it isn't the best treatment option for the patient. Many kidney doctors themselves would likely choose nocturnal in-home dialysis such as NxStage (DaVita is smart and owns part of it).

Yes, I notice all of the suits and investigations in the filings over the years. I think the outcome on most of them seem to be fine. I don't know if there are any big bombs lurking, though.

DeleteCertain industries will just have a lot of these things going on.

And yes, Goldman Sachs, Walmart, Coke, Wells Fargo etc... plenty of Buffett's holdings have all sorts of legal issues.

I'm usually skeptical of a lot of claims (having seen up close some of them that I have a high comfort level with (in finance, for example), but we'll see how DVA's stuff settles...

Yeah, if one is a kidney doctor, one might prefer nocturnal in-home dialysis.

DeleteBut would laymen have the confidence to drain all their blood on their own at home, clean it, and put it back? If they make a mistake, its fatal.

DaVita is "Too Big To Fail". Fresenius and DaVita are like Union Pacific and Burlington Northern - can't do without them.

I have noticed that Buffett has been buying DVA. Your post is a fantastic overview of the stock. Thanks for your efforts.

ReplyDeleteROC is really low...isn't that really bad for a long term stock investment?

ReplyDeleteWhat are you looking at? ROE has typically been in the 20% range and return on capital (equity + lt debt) has been in the mid teens, usually. There is some noise after the HCP merger but they are still guiding towards something like 12% return on capital (operating earnings guidance for full year / Q3-end total capital).

DeleteThanks for reading.

From 2012 annula report: pg. 90 earnings=536 Millions, pg.93 LTD=8,3 Bil and equity 3,7 Bil => 0,536/(8,3+3,7)=4,46% that's really low...What data are you looking?

ReplyDeleteOh, I see. You used net earnings against total capital. In order to compare apples to apples, I would compare net earnings to equity (because net earnings include interest expense deducted for debt) and operating earnings or EBIT to total capital as this is before interest expense (so would not make sense to compare to equity).

Delete...even if we use the definition or ROC=Opereting Income/(end year equity + debt) when in 2012 operating income is 1,3 Bil => ROC=1,3/13=10%...still very low for a company that should have a MOAT...

ReplyDelete..Disclaimer: I don't use neither of the above definition for ROE and ROC but that's not the point of the thread...

ReplyDelete...1,3/12 (not 13)...ROC=10,8%...

ReplyDeleteThe problem with your above calculation is that there was a big merger at the end of 2012 (HCP closed in November). So you are including all of the capital of DVA and HCP combined, but only the operating earnings for DVA since only a month or two of earnings are included in the 2012 figures.

DeleteUsing Greenblatt's return on capital (EBIT / (net PPE + net current assets)), you would get 32% for the first nine months of 2013. Annualzing the first nine, that would be 43%. This would reflect the underlying profitability of the business regardless of capital structure.

A lot of the asset on the b/s is goodwill, so you can look at return on tangible equity too to see what the underlying business looks like (goodwill reflects what they paid in the past for businesses).

So the economics are a little better than you think, but still not great compared to other companies for sure.

Thanks for the discussion.

Thank you very much!!!

ReplyDelete... great observation...I just looked at years 2011 and before...things looks a little better...and I'm going to think and read better the balance sheet...

...return on capital (EBIT / (net PPE + net current assets)...this has important implication I had to think about...good food for thought... :)

ReplyDeleteFor a company that has in the past years shown a consistent acquisition strategy should we expect the same strategy in the future? If yes should ROC consider goodwill?...and with goodwill the ROC is average...doesn't shown a sign of a business with a moat...I hope I'm wrong.

ReplyDeleteYes, that's right. You can't ignore goodwill if acquisitions is a major part of the growth story; it is what they are paying for business so it is capital they are deploying. Return on assets excluding goodwill just shows you how good the business is at the operating level. Plus, it is the potential return from growth through opening of new centers as in that case they are buying real, non-goodwill tangible assets to grow the business.

DeleteSo you do have to look at all of that.

As for moat, that's a good question. HCP is still a big question mark (facing dramatic declines next year) and that was the latest, biggest deal. Hopefully, they clarify their view and plans for HCP on investor day (December 9). I assume they are planning to do what they did with DVA and grow in the same way.

As for DVA, it is a duopoly with Fresenius. Their scale and operational competence is a competitive advantage. I would like to see from them more information on how they are preferable to independents and non-profits in terms of economics and patient outcomes. I think they can do more in that area to make it clear.

Anyway, we shall see how this story develops.

I just looked not in deep the annual report and some datas...so probably i miss something about thei scala advantage. They are big as market share but they don't have big fixed costs (no advertising and marketing, no heavy distribution, no big R&D etc)...the majority of costs in percent of sales seems to be "patient care costs" at 68% of revenue...and of this only the aspect of the acquisition of pharmaceutical can have same scale advantage...I wonder if there is another barrier of entry that I'm missing and that's not about cost advatage due of scale...

ReplyDeleteThis is a typical rollup type thing. I don't have the figures handy, but years ago dialysis was done all over the place, in hospitals, doctors offices, independent dialysis centers, non-profit centers (there is still a large one) etc... And over the years, DVA and Fresenius have bought them up; sellers figured they are better off letting specialists do the work. This has all the usual benefits of best practices, IT systems etc... (good practice at one location can be transferred and learned at other centers etc...).

DeleteThere are still a lot of the above operators, but the trend has been for consolidation. The reason/benefits is not that different from other rollup situations.

As for an actual moat, I think the above is sort of a moat. It's true that anyone can buy dialysis equipment, hire doctors and set up a dialysis center. So in that sense, I suppose there is no real moat. But I think the trend as in many other industries is towards consolidation/specialization for cost/efficiency reasons, for one...

People looking for the DVA moat can find it here. 205 Congressmen signed this wonderful letter to the Center for Medicare Services in August.

ReplyDeletehttp://dropbox.norglobe.com/files/ESRD%20final%20letter---1217271.pdf

BTW, the current Medicare reimbursement situation is a replay of 2004. It seems DVA management was overly conservative back then too.

http://online.wsj.com/news/articles/SB109354586719602084

From the 2004 WSJ article: 'In a recent research note, Gary Lieberman, an analyst with Morgan Stanley, called the company's outlook "unreasonably conservative."'

Thanks for that (and other commentors who linked similar things). This letter makes sense and is what I figured. I think this is different than many other government 'risk' issues; dialysis needs to be funded. It's not like a new fighter or some big defense project that can be cut (without immediate, highly visible and unacceptable damage), so in that sense this is a lot less risky than it looks.

DeleteAs for DVA's posture, I also figured it is part of the game; they can't say everything will be OK. They have to express clearly how damaging any cut would be; if management said it's OK, we'll figure it out, then they would go ahead and cut and not worry etc...

Thanks for the links.

The letter from the 205 Congressmen is linked off of this article

ReplyDeletehttp://www.renalbusiness.com/news/2013/08/house-of-representatives-speak-up-about-proposed-cuts.aspx

Finally, Medicare made only a 0.55% cut.

Delete17 out of 22 Senate Finance Committee members had also written a similar letter (Senate Finance Committee has jurisdiction over CMS).

Their ROC on tangible assets must be astronomical. The ROC on the Value Line chart, although high, is not the full story. Because they have intangibles of $56 per share.

ReplyDeleteDVA is like See's Candy (except See's Candy doesn't have acquisition opportunities)

- Revenue goes up every year (4.4% CAGR of new dialysis patients), insurance contracts are indexed to inflation, Medicare payments are supposed to be indexed to inflation since 2011.

- Maintenance expenditure is less than 2% of revenue (2007 capital markets presentation).

They seem to have paid for all their acquisitions with cash except for Healthcare Partners. They even paid for Gambro with cash (leveraging upto 5.2X EBITDA at the time).

In the first 3 quarters of this year, they already report 8.5% dialysis patient growth over last year (166K/153K).

Why does the stock keep dropping?

Good observations. I agree. A lot of the street is still spooked about the dialysis cuts, I think. My opinion is that folks who worry about that are asking the wrong question. A lot of investing is about asking and answering the right questions.

DeleteThe stock popped when the dialysis cuts were taken back, but the recent decline might be part of an overall stock market decline. Plus, there are big cuts coming to medicare advantage that will hurt HCP.

But even there, I think the street is worried about the short term hit to HCP but don't really think about the long term. In the long term, it is a tremendous area of growth. And the market will be served somehow in some way, just like dialysis will be done by someone, somewhere, and it will be done economically.

Some people are afraid that the government will suddenly enter these businesses post office-like and offer them at a loss and therefore killing the for-profit private entities. Of course, I suppose anything is possible, but to me that goes in the opposite direction of what has been happening over the past, and the pressure to NOT do something like the post office (increasing deficit by offering services below cost) is increasing. So I find that scenario pretty much a zero probability (although nothing is really zero probabibilty!).

Others say that non-profits can cut prices indefinitely and kill off the for-profits. But that too is wrong. "Non-profit" might mean there is no pressure to make profits, but it shouldn't be confused with "infinite funding and resources". Non-profits still have to generate enough revenues to pay the bills. Maybe they get a subsidy (like universities) from some endowment or trust, but for the most part, non-profits have to make the budgets work.

So the argument that the non-profits will destroy the for-profit companies doesn't make sense to me either. As someone said in another post, if a for-profit can be just a little more efficient than the non-profits, they can make tons of money even if non-profits keep operating at break-even. I haven't heard of any non-profits with unlimited funding.

Anyway, I think this is one of those classic situations of time arbitrage, first-level / second-level thinking and all of that.

As for day-to-day or month-to-month stock price movements, who knows?

Thanks for reading.

DVA is favorably mentioned in today's NYT article on ridiculous hospital prices.

Deletehttp://www.nytimes.com/2013/12/03/health/as-hospital-costs-soar-single-stitch-tops-500.html?hp&_r=0

Though they are technically non-profit hospitals, they charge enormous markups compared to for-profit companies for things like blood tests, X-rays etc. In this case, the non-profit profiled did the following

"And, like any business, many hospitals try to do fewer services that are not well paid. In 2012, over loud patient protests, California Pacific Medical Center outsourced its kidney dialysis unit to DaVita Health Care Partners, a commercial company, citing decreasing reimbursement."

The Medicare Advantage cuts are a legitimate one-time hit. Medicare Advantage prices are 12% more than Medicare on average. But that 12% is used by insurance companies to cover vision, dental, hearing (which are not covered by traditional Medicare). The out-of-pocket cost of Medicare Advantage is also far lower than traditional Medicare.

This is why Medicare Advantage has had blockbuster growth - even after the ACA was passed. Traditional Medicare is fee-for-service whereas Medicare Advantage plans are like HMO plans. This ties into what Healthcare Partners calls "fee-for-value".

The Medicare Advantage issue is one of the govt. vs. the private sector debates - i.e. who can do a better job of administering health plans. I think the rapid Medicare Advantage enrollment will continue. Once the govt. cuts away the 12% premium as per ACA, the difference will become more apparent - seniors would continue to choose fee-for-value over fee-for-service - i.e. suppose a Medicare Advantage plan covers vision, dental, hearing in addition to lower out-of-pocket costs compared to fee-for-service Medicare. The govt. then won't be able to justify any further Medicare Advantage cuts.

This is why the DVA CEO repeatedly calls Healthcare Partners a huge opportunity because there is so much wastage. They have applied to CMS to be able to take care of all medical needs of dialysis patients, not just dialysis. If they can reduce waste in other areas of healthcare, like they have with dialysis, there is lot of upside.

BTW, their member growth at HCP has been stellar so far (something like 20% in the latest quarter).

There are Harvard and Stanford case studies on the DVA CEO.

DeleteThere isn't any headroom for the govt. or a charity organization to compete - its like trying to compete with Walmart. DVA pays its patient-care technicians something like 12-14$ per hour (there are youtube videos of the DVA CEO talking at Stanford business school etc., he mentions this rate in his talks).

If the govt. were to try doing dialysis on its own, its costs would be several times higher. It certainly can't pay its employees at that rate.

The DVA CEO has cultivated a unique culture at DVA - he leads chants at company meetings. They are reminiscent of the Obama chants from 2008. He is a very interesting guy. He has had two startups before Davita - one success and one failure.

Yes, I saw that this morning; DaVita mentioned. I like to believe that DVA is on the right side of the solution. If that is the case (which it seems to be), then DVA will come out really good on the other end of this.

DeleteI don't know much about HCP, but it does seem like it can be a huge opportunity.

I know first-hand how inefficient and wasteful health care is... I've been in an emergency room (nothing serious) and I had to fill out the same form multiple times and answer the same question to three different people. I finally got to see the doctor and then what did the doctor ask me? My name, address and insurance provider. I was so frustrated and told him that I already filled out three different forms to answer that question and then told the nurse that was in the room 30 seconds before the doctor showed up... why does he have to ask this question again and then input it into his computer?!

(this is the same frustration with getting help on the phone; I type in my phone number, account number and all of the relevant information and then the operator gets on the call and then asks me, guess what? My name, phone number and account number... I tell the operator that I had just typed that in on my phone, don't they have it? lol... The waste and inefficiency everywhere is insane!).

So I think there is a LOT of room for tons of money to be made by people who are on the *right* side of solving the problem.

http://www.abqhp.com/Documents/News%20Release%20v2%20%2012%202%2013%20FINAL.pdf

ReplyDeleteI don't know how much revenue depends on this, but it seemed significant on their last earnings call.

Are you going to attend their investor day on Dec.9? I saw that you attended the Leucadia annual meeting in New York. If you do, maybe you can ask them why they have been giving ultra-conservative forecasts.

Hi, thanks for the link.

DeleteInvestor day will be webcast, so I plan on listening to that. As for the ultra-conservative forecasts, I think it's just a practical matter; you can't be negotiating with the government and complaining that reimbursement cuts will destroy their business on the one hand and then tell investors on the other that they will make tons of money.

So I think part of it is that. And then, of course, there is real short term risk as we saw this year so there is really no upside to being too optimistic. It's better to assume that surprised will be to the downside etc...

Hi - i'm just looking at your free cash flow numbers... how are you looking at "loss contingency reserve" of $397M for the 9 months ended Sept 30. I believe you are including that in free cash flow... but i'm not sure that is proper given that that money might be out the door any day... would love to hear a clarification - thanks

ReplyDeleteHi,

DeleteThat reserve is for potential settlement on govt investigations and is for something that happened in the past so is sort of like JPM's $13 billion settlement. It would be misleading to put all of that expense in one year; it wouldn't reflect the ongoing, run-rate potential of the business.

So it is OK to exclude these big charges to get a feel for the 'normalized' earnings or cash generating power of the company.

Having said that, it's true that these businesses have legal and regulatory risk so these things will happen every now and then, so we can't assume it all away as one time. But it's certainly not going to be at a pace of $397 mn every nine months, though. Or at least we hope not.

Thanks for reading.

The conclusion of that investigation should boost the stock. Its been going on for more than 2 years now.

DeleteBy my calculations, without the extra charges i.e. ( Operating income - Debt Expense - Taxes ) / Shares, we get $4.29 EPS for 2013.

But all finance websites show $2.66-2.78 EPS for this year due to all these charges.

When that investigation ends, it will clear up the EPS outlook.

Excellent write up.

ReplyDeleteYou might want to bare in mind the net cash payments to non controlling interests when using a market value multiple of "steady state" FCF/share?

Looking at the cash flow statement, what do you make of the significant movements in the borrowings and payments of long term debt? It is a significant multiple of the total borrowings.

Outsides CEO? Worth watching - https://www.youtube.com/watch?v=oRsMIOdR2dc

They never repaid the debt used to acquire Gambro. My guess is they won't repay this time either, they will just get bigger. On the Q3 earnings call, the CEO said that he hopes to buy something nice next year. Second preference is share buybacks and debt repay.

DeleteIt is not the absolute level of debt to which I am referring too. Look at the gross changes in debt in the financing section of the cash flow over the past 6-8 years and compare this to the actual level of borrowings.

DeleteHi,

DeleteGood catch. I didn't deduct minority interest; you are exactly right. If I use free cash flow and calculate that per common share, I have to deduct the payments on minority interest. I might fix and update the table above or just do that in a future post if I put in an updated table.

As for the cash flow movements on debt, that is strange and the figures look unnaturally large. I didn't see any explanation and can't think of anything that would cause such distorted figures at the moment.

Thanks for reading.

Oops, I was going to correct the free cash flow figures, but they turned out to be correct. I got those figures from the DVA press releases. I thought I calculated them myself, but that isn't the case.

DeleteSo the figures in the table are good. They do reflect 'free cash flow' as DVA defines it; operating cash flow minus payments on minority interest minus maintenance capex. So that is fine.

Sorry for any confusion!

I knew (yeah it sounds corny) that Weschler was buying soon after the Q3 earnings call. Because it was a certainty (in my mind at least) that CMS wouldn't cut (would it really oppose the bipartisan majority in Congress asking it to not cut), and the stock didn't drop much despite massive volume.

ReplyDeleteI suspect he might be buying again this week because today again despite larger volume there was a small price drop. Especially in advance of the Dec. 9 investor day.

He seems to be trimming DTV and moving the money to DVA. DTV has too much competition, no Internet service, rising programming costs and its Latin American story doesn't look that great anymore because of the economic problems in Brazil.

Dialysis will be around 100 years from now - like the railroads. But DTV, and for that matter any media company may not be around even in the next 10 years.

Maybe Weschler will sell more DTV and buy even more DVA.

Its very hard to come by info on Davita. Somehow Google doesn't pick it up. I found the ABQ release by accident - by chance i went to the ABQ website! Here is the House hearing on Medicare Advantage cuts yesterday. The Davita co-chairman testified

http://energycommerce.house.gov/press-release/health-subcommittee-finds-health-laws-brokenpromises-will-soon-hit-medicare-advantage-beneficiaries

Robert Margolis, CEO of HealthCare Partners and Co-Chairman of DaVita HealthCare Partners, testified, “The MA program is under severe stress due to a number of cumulative cuts to the program, including reductions to MA plan benchmarks; coding intensity adjustment; changes to CMS’s risk adjustment methodology; sequestration; and the tax on health insurers. Benchmark reductions alone were intended to bring MA to parity with the original Medicare. Additional layered reductions cut deeply into the MA program and flow to patients in the form of fewer physician choices, fewer benefits and increased patient costs. The cuts have the net effect of pushing seniors away from MA and into the fragmented FFS delivery model.” - See more at: http://energycommerce.house.gov/press-release/health-subcommittee-finds-health-laws-brokenpromises-will-soon-hit-medicare-advantage-beneficiaries#sthash.jKxAFpFx.dpuf

Weschler has been familiar with the dialysis industry for something like 20 years. He used to report directly to Peter Grace (CEO of WR Grace). WR Grace bought a dialysis company in the 1990s.

ReplyDeleteI find it strange that people find DVA hard to understand. It is the simplest company I have looked at. For example, Mohnish Pabrai says he could never invest in DVA because he doesn't understand it.

One more interesting article (although this will benefit DVA only in the very long term). I say very long-term because this ESCO program is moving at a glacial pace at CMS. I have pasted an excerpt below.

ReplyDeletehttp://www.denverpost.com/ci_20676856/davita-buys-doctors-network-4-42-billion-bid

DaVita controls about $33,000 in Medicare spending for each dialysis patient, but those clients often are very sick with multiple illnesses and cost about $55,000 more each year in other health needs. Kent Thiry, chief executive of DaVita, says the company could manage the entire $88,000 per patient, saving the government money while improving quality at the same time.

In a conference call on the merger Monday morning, Thiry said HealthCare Partners' experience managing costs and quality for employers and insurance companies will help DaVita's plans. The 1,800 dialysis clinics operated by DaVita are natural locations to add other health care services, the company said. Patients are in dialysis chairs three to five hours, three times a week, and they could use that time on general needs, such as eye and foot exams for diabetes patients.

Thanks for the link. Yes, I really do think there is a lot of opportunity for people who are going to be the part of the solution to the health care problem. There is huge change going on right now and it is very visible. DVA/HCP seems to be on the right side of the problem for sure as we really do have to get costs under control. The old way of doing things is just not going to work anymore...

DeleteA recent example is the flu shot. Until recently, we had to go to the doctor to get a flu shot and it was very hard to get an appointment. It's just a flu shot. Why does some highly qualified, trained doctor have to waste his time giving flu shots? Now anyone can walk into just about any CVS or Walgreens and a nurse or someone will give you the flu shot right away. It's insane that we all had to wait in line at the doctor's office to get some simple procedure like this done; waste of valuable resource (doctor's time), waste of money (expensive) etc...

So I think there is a lot of room for things like that.

I don't know anything about it, but I think Graham Holdings (old Washington Post) bought some kind of healthcare company too; one that promises to take care of patients cheaper etc...

I think it's a huge area with a lot of potential.

The DVA CEO says health exchange dynamics are a risk. When the analyst on the call asked whether any health exchange plan rates are lower, the CEO replied that so far all health exchange plans are at commercial rates. This is another example of how over-cautious he is.

ReplyDeleteIt seems to me that if DVA and Fresenius are both unified in not accepting lower rates, insurers really don't have leverage. Because these 2 companies together have 75% marketshare. An insurance company can't really leave out these two companies and claim any sort of viable dialysis coverage in any given geographic area. Unless patients drive hundreds of miles.

It seems to me that DVA and Fresenius don't undercut each other on price - when I read the earnings call of Fresenius, they too are always trying to get higher pricing. Therefore an insurer cannot play these two against each other.

But the DVA CEO did mention that a smaller dialysis competitor was cutting price for higher guaranteed volume. Not sure how this works - can a small dialysis player say that after 30 months (i.e. once Medicare kicks in) all patients have to go elsewhere? Not sure if that would be legal or palatable to CMS, because the implicit understanding is that Medicare takes over after the first 30 months, but until then insurance companies have to pay a high price to support everything.

Over time this should get sorted out in DVA's favor. As DVA and FMS keep growing marketshare, their leverage with insurance companies only increases.

Patient numbers by dialysis provider are at this link

http://www.nephrologynews.com/articles/109621-moderate-growth-for-providers-but-rebasing-aco-participation-will-impact-long-term-picture

The third largest dialysis company has only 13,954 patients - Davita has 157,000 and Fresenius has 164,561. This was May 2013 data - as of September 2013, Davita had climbed to 166,000 patients.

So if both Davita and Fresenius don't give in on pricing, there is precious little any insurance company can do. However, as one would have expected the Davita CEO was over-cautious about this too in the Q3 earnings call.

Forgot to mention that the DVA CEO said that they won't accept a lower rate, so if an insurer bargains, they would have to go somewhere else.

DeleteBofA Merrill Lynch has DVA among its top 10 buys for 2014 (link below). Looks like the analysts like it (I think it was the William Blair analyst who said after the CMS decision 2 weeks ago that investor expectations were "abysmal").

ReplyDeleteBuffett said his successors should understand both human and institutional behavior. The human behavior is well documented. The institutional behavior seems harder to learn about.

Maybe its a 1972-type 2-tiered market? Or maybe every institution waits for someone else to make the first move?

http://247wallst.com/investing/2013/12/06/merrill-lynch-unveils-its-top-10-stocks-to-buy-for-2014/?source=email_rt_mc_body&app=n

Very interesting investor day - transcript is on seekingalpha.

ReplyDelete1. It seems they signed an agreement a couple of days ago with the insurer they had referred to in their Q3 call. Kent Thiry said both sides were not happy with it - I interpret that to mean the rate increase was not big enough :).

This is a number that Thiry mentions from time to time - 77% of all dialysis clinics are owned by investors - and therefore pricing is rational. Looks like its indeed the case.

2. Thiry also said that he would be disappointed if HCP doesn't move into 2 more states in 2014, 3 more states in 2015 and lot more after that. He said the only thing that has slowed them so far is that they do not have enough business development people. He said the opportunities are "mouth-watering", but he does not have enough deal-makers.

3. Thiry wants people who have private insurance to be able to keep it even after they get ESRD if they want to - right now they are mandatorily moved to Medicare after 30 months. He expects it will happen, but can't predict when. What started out as 0 months, became 12 months, then 18 months, then 30 months, to reduce the burden on Medicare. But he has been talking about this since at least 2007.

4. VillageHealth has produced 15% savings on non-dialysis Medicare expenditure i.e. they can save 1.2% of the entire Medicare budget (8 * 15%).

5. DaVitaRx results in 13% fewer hospitalizations - just because the patients otherwise don't take their pills regularly!

Hi,

DeleteYeah, I listened to the presentation and read the transcript too. It sounds pretty good. Maybe short term iffy, but long term good.

What did I tell you - Berkshire was indeed buying last week as I had thought. They bought 1.3 million shares last week.

ReplyDeleteI had posted a comment above on this page on December 6 (1:28 am) and it turned out to be true.

http://brooklyninvestor.blogspot.com/2013/11/davita-healthcare-partners-dva.html?showComment=1386311309713#c7044342671856565800

Here is the Form 4 link

http://www.secform4.com/filings/927066/000118143113062025.htm

Totally, they have bought 5 million shares in the last month. They now own more than 17% of Davita.

But you cannot find this off SEC Edgar. I had to google for it based on my guess. If you go to SEC Edgar and search for "Berkshire Hathaway", you cannot find this form 4.

You were right; good call. That's a pretty big ownership stake.

DeleteBy the way, you can find the form 4s at SEC edgar; you have to click "include" on ownership filings at the top. I think the default might be on "exclude" because sometimes you have a whole bunch of form 4s that you can't find the regular filings.

DeleteDo you think they will acquire DaVita during a bear market? So far, they have 17.1% of Davita. Weschler has an additional 1.1% in his personal portfolio. I haven't seen them negotiate a standstill agreement with anyone other than Burlington Northern. In the Q3 call DaVita said that it was Berkshire which initiated the agreement and not DaVita.

ReplyDeleteThey had an agreement with Burlington Northern that they wouldn't acquire more than 25%. Once they bought 22%, they paid just a 30% premium in October 2009 for the rest. At that time, everyone thought we were in a bear market rally and nobody thought the 30% premium was low. It was a great price in retrospect. Of course, Buffett had a train journey (from Texas to Chicago IIRC) with Matt Rose (CEO of Burlington Northern) before the acquisition.

Hi, I have no idea about brk buying all of dva. It has certainly been rumored, but I don't have any particular insight into that. Thanks for reading.

ReplyDeleteThere is lots written about the dialysis business but very little about Healthcare Partners. This is a different business, a large part of the total revenues and profits, and "where the puck is headed" so needs careful consideration. The capitation basis of reimbursement takes on a lot of risk. Do you have a view on this?

ReplyDeleteHi,

DeleteThat's true. There is a lot of historical data on dialysis so it is well understood. HCP, not so much. If you listen to the capital markets day conference call, though, it sounds pretty good.

There is a lot of risk there, of course. But it's like anything else, like banking (credit risk), insurance (cat risk), health insurance etc... So it's all about management and 'underwriting'. What was encouraging from the CM day, I think, was that despite far larger than expected cuts in HCP, they are expected to make positive cash-on-cash returns.

Like any other business, it's a business that needs to be done so I don't worry about prices perpetually going below cost of delivery.

As for arbitrary pen-flicking in DC destroying the business, I don't worry about that too much (except in the short term) as HCP seems to be in a business that will need to get done and if they can do it better than others there will be business for them.

But again, we don't have a whole lot of historical data to confirm this (as we do with the dialysis business) so we will just have to see.

Thanks for reading.

This discussion of DVA reminds me of another healthcare stock I've been researching, Quest Diagnostics. Quest is the largest diagnostic lab company in the U.S. even though it has only 8% market share (the market is highly fragmented with many small players). Medicare reimbursements are scheduled to fall slightly over the next few years and the stock has gone down over the past 12 months. The company has not allocated capital well in recent years as it has overpaid for acquisitions that haven't worked out as planned. But the company hired a new CEO last year who has stated future acquisitions will be limited and the company will focus on improving operations internally and directing cash towards dividends and stock buybacks. The CEO came from a division of Phillips Healthcare so he has no public track record. It is too early to judge his performance, but in just the past two quarters the company has spent over 10% of its market cap buying back stock (granted, this was funded partially with a divestiture). Like DVA, if reimbursement cuts deal a blow to the industry, Quest (and LabCorp) could do alright in that environment as smaller, higher/cost independent labs suffer disproportionately. The best thing about the company is that is has had unbelievably stable profit margins over the past decade and it currently trades at a double digit free cash flow yield (CFO - cap ex - minority distributions).

ReplyDeleteI just found your blog and really enjoy it. I stumbled across it while searching for information for Post Holdings (which I own). You do great work. Thanks.

Hi,

DeleteThanks. And yeah, Quest is an interesting company. I've looked at it now and then over time but never owned it. Maybe I'll take another look. I do like the stories of uncertainly causing trouble for the smaller guys and big guys just scoop up the business.

Thanks for reading.

Did anyone figure out the craziness in the cash flow statement (Borrowings/Payments line in Cash Flows from Financing Activities)? I emailed IR and they didn't respond.

ReplyDeleteHi,

DeleteGood question. I haven't heard anything about it, and it seems to never come up in conference calls / analyst day Q&A. It is odd.

What do you think about the fact that the CEO has no significant stock ownership and that he is extremly overpaid?

ReplyDeleteI don't mind the pay so much as long as he performs. But yes, it would be better if the CEO owned more stock. But some people just don't own a lot of stock; they sell and find other things to do with their capital; like Munger.

DeleteIf I remember correctly he had something $26 Mil for a company that had $1.2Bil in FCF...he is more paid than the CEO of Well Fargo (earning around 19 Bil)..he is more paid than the CEO of IBM..and the CEO of Coca Cola...his paycheck is really embarrassingly high .

ReplyDeleteJust out of curisosity where do you put the line? How much he can increase his paycheck before you say "Ok this is too much!"

He is not just not owning a lot of stock...he just don't own any.

ReplyDeleteLast year's proxy shows him owning around 715,000 shares (proxy is dated May 2013). There was a 2:1 split in September so he would own 1.4 million shares; that's almost $100 million so that's not nothing.

DeleteAs for CEO compensation, I have to admit that I have not been too picky about that in the past and I know that's not a good thing. I should pay more attention to that sort of thing. But it's hard sometimes to compare these things across businesses and industries. $26 million sounds big, but he has created billions in shareholder value too. But yes, it is strange that he makes as much as Jamie Dimon, one of my favorite CEOs in one of the toughest jobs out there, I think.

My primary focus (as you can tell from my posts) is the business model and performance of the CEOs, and I look at their results *after* compensation etc... usually. And if they are performing well after these expenses, I am fine with it.

Again, I know this is not the most responsible way to look at things, but that's just me. I tend not to overly focus on that sort of thing even though I should.

Another example was when people were saying that the 50% incentive fee at some hedge funds were ridiculous. Well, for me, I don't care what the incentive fee structure is. What counts is the return after all fees, right? I would rather pay someone 50% incentive fee and earn 20% after all fees than pay some mutual fund company 0.8%/year to underperform the S&P 500 index year after year.

So I think the result is what counts in the end.

If Thiry doesn't perform and still pays himself too much, I hope the board acts responsibly, and they don't, hopefully some activist shareholder will come in and fix the problem.

Anyway, I know this is not a great answer... sorry...

Thanks for reading.

First thank you very much for your insights.

ReplyDeleteYou are right and I was wrong, I didn't consider the stock split...he has about 4X his income in stocks...that's something...could be way better but it's something for sure.

...looking here it seems he has way less http://finance.yahoo.com/q/mh?s=DVA+Major+Holders ...

ReplyDeleteThe proxy generally include also stocks that the management don't have (potential stock option)....

Any suggestion on the easies way to find the right numbers? ...yahoo for a fast answer and the proxy (exluding the option) for an in deep info?

Hi, I usually just look at the proxy. You can read the notes to back stuff out, I guess. Otherwise you can just look up the form 4's at sec.gov.

DeleteHere's Thiry's from May 2013:

http://www.sec.gov/Archives/edgar/data/927066/000118143113028062/xslF345X03/rrd379960.xml

finviz.com + at the end of the page...numbers of share and relative form 4...

ReplyDeleteThank you...132,775 X 2 X 66 = about $17.5 Mil... ( hope I'm right )

ReplyDeleteHLS seems to fit the bill for a similar situation w/ a healthcare company. Once upon a time, several divestitures and one accounting scandal ago they were a hospital behemoth. Now they are the largest IRF (inpatient rehab facility) network... meaning they do rehab for people who have suffered from strokes, broken hips, etc and need to learn to take care of themselves again. 80% of IRFs are attached to acute care hospitals and are unprofitable b/c the specialized staff members (therapists etc) are under utilized by a patient base limited by the hospital. HLS on the other hand has mostly free standing facilities that can take patients from several area hospitals leading to higher utilizations and~20% EBIT margins. Over the last few years they have paid down debt, increased FCF, and recently started returning that FCF to shareholders in a meaningful way.

ReplyDeleteThanks. I'll have to take a look at that.

DeleteThanks for sharing your thoughts with us.. they are really interesting.. I would like to read more from you.

ReplyDeletetrain your pelvic floor

Interesting blog and I really like your work and must appreciate you work for the health and and fitness.

ReplyDeleteRaw and living foods

I was really want to get some more detail and information about the health, body care and clinic but your blog helped me so much thank you for sharing it.

ReplyDeleteskincare drugstore products CVS

Your blog provide a very interesting and help information about the fake medicines kill i agree with it.

ReplyDeletefake medicines

Very informative article which is about the health and fitness and i must bookmark it, keep posting interesting articles.

ReplyDeletelose 5 kilos in 5 weeks

All the information are very nice well done and keep posting.

ReplyDeleteZero Up

Such a nice blog and very nice you work and sharing this wonderful article about the Cutting Edge Online Training.

ReplyDeleteCutting Edge Online Training

Very interesting and informative blog and about the results-driven skincare and I must appreciate your work well done keep it up.

ReplyDeleteresults-driven skincare

Most valuable and fantastic blog I really appreciate your work which you have done about the environment,many thanks and keep it up.

ReplyDeleteenvironment

Glad to read your informative post, keep sharing valuable information! Looking forward to seeing your notes posted.

ReplyDeletetype 2 diabetes symptoms

Thanks for sharing this amazing blog and the details about enfermedad de pian really awesome.

ReplyDeleteGood work.

enfermedad de pian

I have read many blogs but your blog are always very nice and now here I got some detail about the Child Development Center it's a Good work keep it up.

ReplyDeleteChild Development Center

Very interesting and informative blog and about the weight loss and I must appreciate your work well done keep it up.

ReplyDeleteweight loss

Well we really like to visit this site, many useful information we can get here. ecommerce platforms

ReplyDeleteThanks for the post. I am very glad after ready and get useful information about the health, body care, and fitness etc., from your blog.

ReplyDeletemedia guides